The S&P 500 Index fell 12% yesterday after a weekend full of bad news surrounding the coronavirus and its spread. This health crisis is rapidly turning into an economic crisis.

A lot can happen in three weeks

In a report published 3 weeks ago, MTN Consulting concluded that vigorous consolidation in the vendor market was likely for 2020:

“As enticing as 5G may be, many factors are holding back a telco capex surge right now, including supply chain issues surrounding China-U.S. trade and Huawei, as well as business model uncertainties around how telcos will monetize 5G. The rest of 2020 is likely to be challenging for vendors, as telcos continue to slim assets, share networks, deploy more software, embrace open networking, and delay or downsize major network upgrades pending a more certain investment climate…Add in the coronavirus, which is already impacting telecom supply chains, and 2020 is looking like a potentially bleak year for the vendors selling into the telco market.”

Since the “Bumpy road ahead for 5G transition” report was published, coronavirus has spread rapidly throughout the world. While several Asian countries have gotten it under control, the US, Canada, and most of Europe has shut down normal life to slow the spread and avoid healthcare system overload. In the US, the social distancing, quarantines and curfews that initially seemed like short-term necessities are now looking like they may be long-term solutions until a workable vaccine is produced. Everyone is being encouraged to work from home (WFH), and students are being forced into online learning as schools close. This is unprecedented. As author Stephen King tweeted yesterday, “This is going to change America, long-term.”

Stay healthy, keep your company afloat, and prepare for the long term

Given the highly contagious element of coronavirus and its relatively high mortality rate, everyone should be first and foremost concerned with health and safety issues. But business leaders also need to keep their eyes on the horizon, to consider how their companies can escape this crisis afloat and prosper in the long run.

As coronavirus lingers, both telecom operators and their suppliers are going to see demand erosion. This could be severe in the next 6-12 months. Many companies in telecom will struggle to survive during this period, even with government stimulus. It’s hard to know how bad it will get. As a NYSE trader said yesterday, “It’s very hard to model what that real impact is going to be… because it’s going to be very large.”

Based on current trends, a few things will likely happen to telecom in 2020:

telco revenues will fall in most countries, along with consumer spending overall

major telcos will layoff staff in the thousands

telco capex will decline in 2020 by 5% at minimum

mobile operators will stretch their 4G networks, and slow 5G network deployment rates

telcos will actively lobby for state relief on multiple fronts, from subsidies to antitrust review of mergers to reimbursement for Chinese vendor rip and replace efforts

Some governments, including the US, Canada and most of Europe, will consider massive stimulus projects in areas like physical infrastructure – in particular fiber construction – but most support will take 1-2 years to materialize

China’s government will double down on state support for its tech sector

Based on this likely path, there will be severe pressure on many vendors selling into the telco market. That’s where M&A comes in.

Consolidation will pick up once markets stabilize

MTN Consulting tracks quarterly revenues for over 100 vendors, with a focus on those selling into the telecom network operator (TNO, or telco) market. As part of this, we track entry and exit into the market, as well as M&A among vendors. In the telecom vendor space, M&A is an ongoing reality – a way to enter new markets, and to improve your cost position. Huawei’s nonstop growth has added pressure on others to team up, as with Nokia’s 2015-6 acquisition of Alcatel-Lucent. Even though M&A often fails, it often appears to be the only option for a company under pressure.

Looking ahead to 2020, a number of vendors will be hit hard by the inevitable downturn facing the telecom market. Those vendors most at risk are the ones highly leveraged to the telco market, as telco spending may take a deep cut in 2020. Other signs of vulnerability include relatively low operating margins, limited cash reserve, and/or high debt loads. Some of the companies that have weak spots going into the coronavirus downturn are shown in Table 1, below. Potential problem areas are shaded red.

Table 1: Select telecom vendors and their financial position as of 4Q19

Company

4Q19 revenue (M)

Currency

Telco/total revenues

Operating margin

Cash months of opex

Net debt to Revenue*

Adtran

116.0

USD

100%

-12.1%

2.47

(0.71)

Aviat Networks

56.0

USD

47%

-1.8%

2.00

(0.52)

Casa Systems

113.0

USD

100%

8.8%

3.32

1.58

Ceragon Networks

286.0

USD

80%

2.8%

0.26

(0.03)

CommScope Holding

2,299.0

USD

82%

-14.7%

0.68

4.02

Infinera

385.0

USD

87%

-15.6%

0.73

0.65

Kudelski

208.0

USD

48%

-0.5%

1.77

1.87

Ribbon Communications

161.0

USD

71%

13.0%

0.96

0.09

Technicolor

1,033.0

Euro

51%

-0.1%

0.23

1.18

Sources: FT, MTN Consulting *Net debt = total debt minus cash & short term investments.

Several companies in Table 1 face a challenging 2020. Two are US-based companies still recovering from major acquisitions, CommScope Holding (ARRIS) and Infinera (Coriant). These vendors focus on connectivity/cabling and optical transmission, respectively. The other two, Kudelski and Technicolor, are European companies with exposure to the media segment and cable television, in particular. In addition, several of the companies in Table 1 are highly exposed to a single product market within the telecom space: microwave for Ceragon and Aviat, access for Adtran and Casa. Diversification can help in a downturn.

Telecom’s two biggest (publicly traded) vendors are not included in Table 1. Nokia is probably the subject of the most M&A rumors nowadays, due to a relatively slow start in 5G commercial rollouts. Nokia benefits from its US ties, though, as well as its good position outside the telco vertical, in transport, energy and government networks. By contrast, Ericsson gets almost all its revenues from telcos, and has bet big on a quick 5G uptake. Given both companies’ broad exposure to telco spending, though, 2020 will be a jittery year for both vendors.

The fifth generation of wireless technology (5G) is steadily growing in the Kingdom of Saudi Arabia (KSA). During 2019, all three operators launched 5G service and are continuously increasing its coverage. The next major step for KSA, which the world is watching closely, is the development of cost-effective and viable 5G in vertical industries such as oil and gas, marine navigation, and connected cars.

Recommendations

While KSA is an early leader in 5G, the following steps can be pursued to improve the commercialization of 5G in KSA:

Develop a long-term roadmap to shutdown 2G and 3G services.

Subsidize the cost of 5G devices.

Enable vertical markets for 5G in consultation with relevant stakeholders. Provide a near term deadline to shutdown 3G services

KSA Overview

Saudi Arabia, officially the Kingdom of Saudi Arabia, is the world’s 13th largest country by geographical area. The kingdom is bordered by Jordan and Iraq to the north, Kuwait to the northeast, Qatar, Bahrain, and the United Arab Emirates to the east, Oman to the southeast and Yemen to the south and it is separated from Egypt and Israel by the Gulf of Aqaba. It is the only nation with both a Red Sea coast and a Persian Gulf coast, and most of its terrain consists of arid desert, lowland and mountains (Figure 1).

Figure 1

Source: Nations Online Project

The Saudi economy is the largest in the Middle East and the 18th largest in the world. It also has one of the world’s youngest populations; about 40 percent of its 34.5 million people are under the age of 25. And, it also has one of the world’s highest immigrant population, about 30% of total. Immigrants account for around 70 per cent of the employed population and 80 per cent of the private sector workforce.

Telecom Market Overview

Government

The Ministry of Communications and Information Technology (MCIT) oversees all information and communication technology matters in the Kingdom. It sets up policies and supervises ICT activities to contribute towards the socio-economic development of the country and citizens.

The regulator, CITC (Communications and Information Technology Commission) is responsible for regulating the affairs of the ICT and postal sectors in the Kingdom. CITC aims to create a highly competitive environment, provide excellent services to subscribers, and establish an attractive ecosystem for investors. It is also responsible for issuing ICT licenses (telecommunications licenses; radio frequency licenses; numbering licenses; and equipment licenses) and monitoring license obligations.

Telecom Operators

STC, Mobily and Zain Saudi Arabia are the three long-established mobile network operators (MNOs) in the country. The state owned and incumbent operator STC founded in 1998 lost its monopoly to Mobily in 2004. Zain, newest to the market, started its operations in 2008.

The mobile telecom sector has more than 42 million subscribers led by STC followed by Mobily and Zain respectively. Virgin Mobile Saudi Arabia and Lebara Saudi Arabia operates as MVNOs in the Kingdom. They utilize the infrastructure and radio spectrum of the MNOs to provide services.

STC and GO Telecom are the two fixed telecommunication licensed entities in the Kingdom.

Infrastructure

Fiber Optic Networks

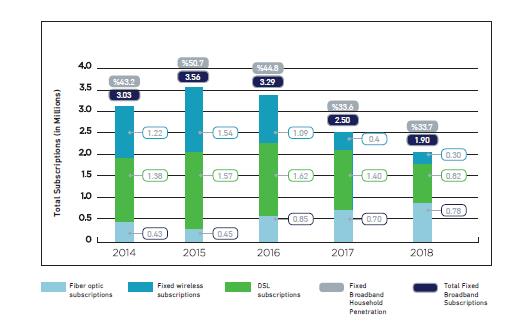

Fiber optic penetration is on the rise due to vigorous efforts of the government and the industry since 2017. According to the MCIT two million urban dwellings were covered with fiber optic networks (FTTx) at the end of fiscal year 2018, with 0.78M subscribers or nearly double the 2015 total. Overall subscription for fixed broadband service stood at 33.7% of for the same period. (Figure 2).

KSA is a member of the 21 member-state Arab Satellite Communications Organization. ARABSAT is a satellite operator that provides broadcasting and telecommunication services across the Middle East, Africa and Europe. KSA has so far launched 16 low-earth orbit satellites.

Submarine Cable Connectivity

KSA is considered as an important hub for submarine networks in the Middle East region, along with the UAE, Oman and Qatar. As of now, there are 13 in-service submarine cable systems connecting the Kingdom to neighboring countries as well to other continents.

Spectrum

KSA’s three operators have been offering 2G, 3G and 4G using a variety of bands. 2G is primarily offered through 900 and 1800, 3G via 2100 while 4G is running on 1800, 2300 and 2600 MHz frequency bands.

5G in KSA

KSA is one of the early adopters of 5G in the Middle East. One key reason is the concentrated effort made by both government and industry in its development. For instance, during the initial period of 2018, the government established the National 5G Task Force to speed up the availability of 5G. It also increased regulatory certainty through the Unified License scheme and released a sizeable amount of spectrum. Furthermore, in February 2019, the MCIT released an additional 400 MHz in mid-band (3.5 GHz) spectrum, taking the combined spectrum available for mobile services, including 5G, to around 1,000 MHz.

Operators have been deploying 5G after successfully completing trials. Zain has so far launched commercial 5G services in 27 cities, STC is deploying 5G home broadband services in a number of cities while Mobily has signed a memorandum of understanding with Huawei for the development 5G in the Kingdom. Zain has also recently launched 5G roaming service between KSA and Kuwait.

Huawei, Nokia, Cisco and Ericsson are all important players in providing the required radio access and core infrastructure for KSA’s 5G rollouts. For instance, STC says that it has blended Huawei and Cisco core networks with Ericsson and Nokia radio access networks.

Key Challenges – 5G

The KSA’s key challenge is the commercialization aspect of 5G in conjunction with the heavy baggage of 2G, 3G and 4G networks.

The second, smaller hurdle – directly connected to the first one – is the availability of affordable 5G devices in the market. The current cost of a 5G device hovers around US$1,000 (~SAR 3,500). Close to 50% of the immigrant population is low-skilled and employed in low-paid jobs and thus are not eager to join the 5G bandwagon, at least in the near future.

The third hurdle will be the enablement of 5G in vertical markets. The list of stakeholders is long and complex. With many open as well as clandestine political agendas, it won’t be easy to come up with a solution. The concerned governmental agencies along with the corresponding industries (education, finance, health, maritime, telecommunication, tourism, transportation, etc.) will eventually face an uphill battle.

Recommendations

KSA is one of the richest countries of the world with a GDP per capita of over $23K at the end of 2018. The IMF expects the KSA economy to decrease by 0.2% in 2019 and grow by the same amount on average per year through 2024. In the telecom sector, the state-controlled structure has landed the operators in a reasonable financial state. With little possibility of any structural change and enough spectrum for 5G, the existing operators as compared to many other markets have few things to worry about, at least in the near term.

At the same time, to further streamline the process of effective and meaningful commercialization of 5G, the following steps can be considered by the government and the industry:

2G and 3G Services Shutdown: A long-term roadmap is needed to shutdown 2G and 3G services. 4G has been available since 2011, and 5G’s penetration throughout the kingdom will grow significantly in coming years. Thus it is prudent to have an effective plan to shut down 2G and 3G networks. At the same time the immigrant population (particularly the low-paid and /or low-skilled segment) has a high tendency to save money for families in their home countries. Thus they prefer cheaper 2G/3G phones over more tech-savvy and high-end devices. Regulators and operators should jointly consider developing a detailed roadmap for the discontinuation of 2G/3G services. It will free up capacity, reduce the number of network elements, reduce carbon footprint, reduce operators’ annual license costs, and allow spectrum to be returned to the regulator or to be reused for 5G if possible. In a nutshell, it will improve networks’ quality of service and the overall financial health of operators. Transition issues such as QoS (quality of service) degradation and vendor contract renegotiation are manageable.

5G Device Cost: Operators may further increase their due diligence with the device suppliers to lower the cost of 5G devices to attract the low-paid immigrant population. The current cost of a 5G device in KSA hovers around US$1,000 as compared to $10-$30 for 2G/3G phones.

Vertical Markets: The success of 5G to a large extent depends on its enablement in vertical industries. An effective roadmap is needed to strengthen 5G in IoT (Internet of Things), AI (Artificial Intelligence), and V2X (vehicle to everything – connected cars) markets.

– end –

Source of feature image: Kemo Sahab (location: Al Bahah, Saudi Arabia)

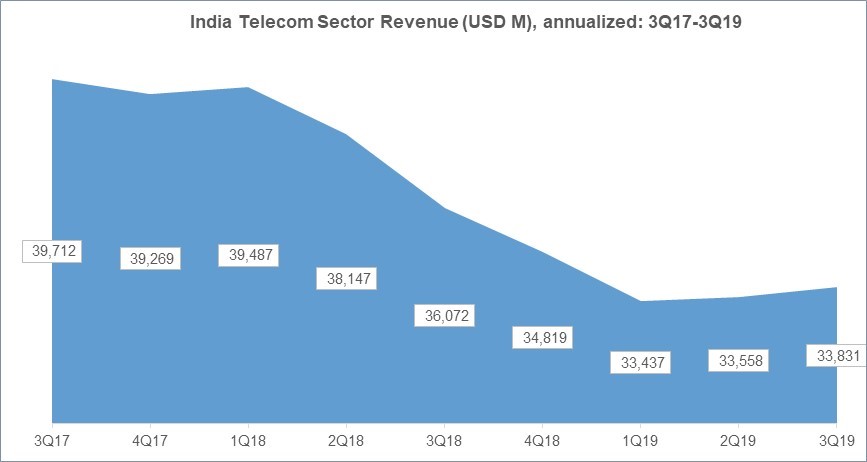

The Indian telecom sector is left in tatters following the Supreme Court’s verdict that supported the Department of Telecommunications (DoT) in a dispute with the telcos over how levies are calculated. Already ridden with massive revenue declines (Figure 1) and a collective debt of almost INR7,800B (US$110 billion), Indian telcos have little cash left for future investments including the upcoming 5G spectrum auctions.

Figure 1

Source: MTN Consulting

Airtel and Vodafone-Idea are under severe financial stress, with the latter on the verge of bankruptcy

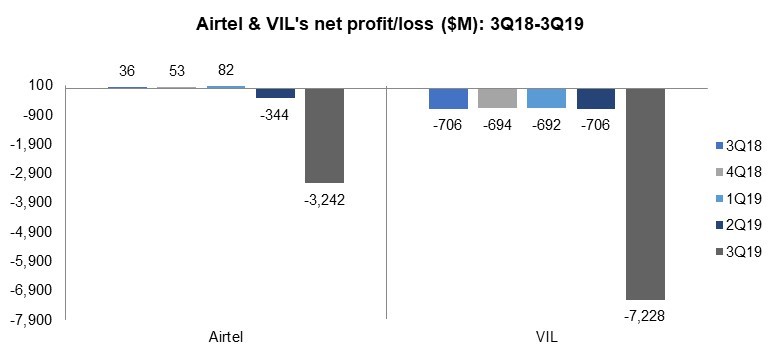

The court’s verdict on adjusted gross revenue (AGR) had significant financial implications on Airtel and Vodafone Idea Limited (VIL). In 3Q19, these two telcos reported combined losses of about $10.5B (Figure 2) as they set aside funds towards AGR dues.

The debate over AGR definition between the DoT and the operators goes back to 2005. The AGR definition is crucial as it has massive financial repercussions for both operators and the government. For instance, the telcos are required to pay 3-5% of the AGR towards spectrum usage charges, and nearly 8% of AGR as license fees.

DoT considers revenues from core and non-core business as AGR, while operators argue that AGR should include revenue only from core business and exclude revenues from dividend, interest income or gains on the sale of assets. Now with the Supreme Court verdict favoring the government’s stance, Airtel and VIL are liable to pay INR216B ($3B) and INR283B ($3.9B), respectively, towards AGR dues. For context, Airtel’s 2Q19 revenues amounted to $2.98B while VIL recorded $1.62B; AGR is significant for both.

Figure 2

Source: MTN Consulting

The liabilities incurred by the operators are huge mainly due to the interest and fines levied since 2005. With both operators already reeling under financial stress amidst the rapid growth of rival Jio, the operators’ strategy to hike prepaid tariffs does not come as a surprise. In the first week of December, Airtel, VIL, and Jio all hiked rates on prepaid plans by more than 40% and are in talks with TRAI to set up a floor price, a minimum tariff for mobile voice and data services. Jio’s decision to join the bandwagon of hiking prices could be the first sign of stability in the sector that has been battered for almost three years.

While both Airtel and VIL are in trouble, Airtel has more options. It plans to raise $3 billion to pay the government, which could involve the sale of its stake in its tower arm Bharti Infratel. VIL has not made clear its plan. It is precariously placed with piled up debt and huge subscriber losses. VIL’s debt to equity ratio increased from 181% in 3Q18 to 487% in 3Q19 (Figure 3). Further, VIL’s subscriber base declined to 311M subscribers in 3Q19 compared to 422M a year back. VIL’s parent entities Aditya Birla and Vodafone are also shying away from making additional investments in the merged entity. With mounting losses and no backing from the parent groups, chances of revival for VIL are low. An urgent sale to a rival operator is possible.

Jio is getting stronger amid Airtel’s and VIL’s financial crisis

Reliance Jio (Jio)’s entry into the telecom sector in 2016 has come down hard on established players like Airtel and VIL. Post Jio’s entry, the industry witnessed intense price competition setting off a sector wide consolidation resulting in just three private operators. Unlike Airtel and VIL, Jio has not been impacted much by the recent court decision on AGR. Jio’s total fine amounts to just $1.8M, given that it started operations in India only three years ago. Moreover, Jio’s parent company (RIL) is forming a new subsidiary that will hold its digital and mobility businesses, including Jio, and transfer all of Jio’s pending liabilities to other divisions within RIL. Post this restructuring process, Jio will be net debt-free with just spectrum related dues to pay. All of this helps Jio manage its cash flows better and will place Jio in a strong position with enough cash to fund for the upcoming spectrum auctions.

So, what lies ahead for the sector?

The next few quarters will be a testing phase for Airtel and VIL, as they seek relief measures from the government to stay afloat. Amid the AGR issue, the government decided to defer spectrum auction installments due from the telcos in FY21 and FY22 by 2 years. This is just a temporary relief, though, and it relates to older spectrum purchases – these operators need fresh spectrum for 5G.

The AGR ruling will be a major hindrance in the telcos’ ability to take part in 5G auctions. For instance, the current suggested base price for 5G is marked at INR4,920M ($69M) per Mhz, with a minimum sale of 20 MHz blocks. This would mean investing around INR100B ($1.4B) for 20 Mhz. The recommended price for the same band in countries like Korea, Spain, the UK and Italy is up to 6 times cheaper. For India’s telcos, spectrum cost constitutes a significant portion of total capex. Considering their financial woes, Airtel and VIL might not even bid for the upcoming 5G auctions at the current price.

Unavailability of adequate spectrum is a related concern. The Indian regulator had put up 300 Mhz of spectrum in the 3.3-3.5 Ghz bands, however with 125Mhz set aside for defense and space organizations, the telcos are left with just 175Mhz spectrum to bid for. Scarce resources get expensive quickly. To help address this, a minimum 100 Mhz block should be assigned per operator for better 5G enablement and deployment, but freeing up this much spectrum will be a challenge.

To justify future investments in 5G, both in spectrum and network infrastructure, telcos will also have to command significant pricing power in new 5G services, which currently seems unlikely.

Unlike many other countries in the MENA (Middle East and North Africa) region, 5G services are already available in the United Arab Emirates (UAE). Etisalat and Du, UAE’s only two operators, are both deploying 5G on the 3.5 GHz frequency band. In May 2019, Etisalat became the first operator in the MENA region to commercially launch 5G service.

Recommendations

For effective commercialization of 5G, operators should focus on device costs and finding ways to subsidize the cost if needed. For their part, government administrators should consider the following:

Provide a near term deadline to shutdown 3G services

Provide a longer-term deadline to shutdown 2G services

Put a strong emphasis on enabling vertical markets

Ease regulations for new entrants

UAE overview

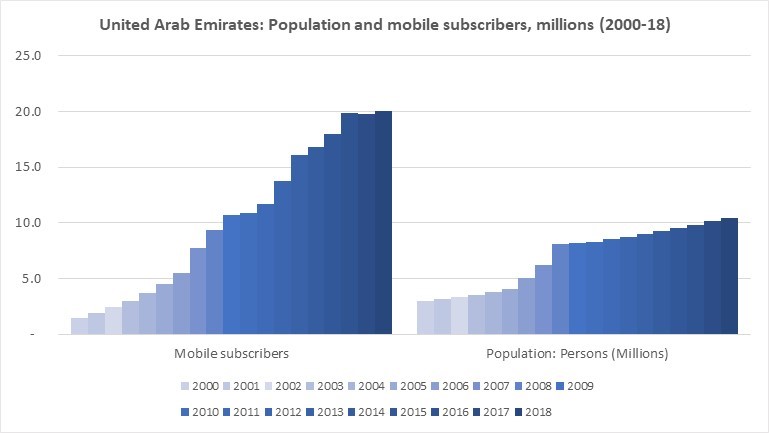

The United Arab Emirates or UAE is at the southeast end of the Arabian Peninsula on the Persian Gulf, bordering Oman to the east and Saudi Arabia to the south and west. It also shares maritime borders with Qatar to the west and Iran to the north. UAE is a federation of seven emirates consisting of Abu Dhabi (the capital), Ajman, Dubai, Fujairah, Ras Al Khaimah, Sharjah and Umm Al Quwain (Figure 1). UAE has one of the world’s highest percentage of immigrants: more than 70% of the overall population. At the end of 2018, the UAE’s population was 10.4 million, up from just 3.0M in 2000 (per the IMF).

The Telecommunications Regulatory Authority or TRA is the federal telecommunications regulatory agency of the UAE. It was established in 2003 to regulate the Information Communications and Telecommunications (ICT) sector. In 2013, its role was extended to include responsibility for the overall digital infrastructure in the country. TRA is also responsible for representing UAE in the international ICT forums.

Telecom Operators

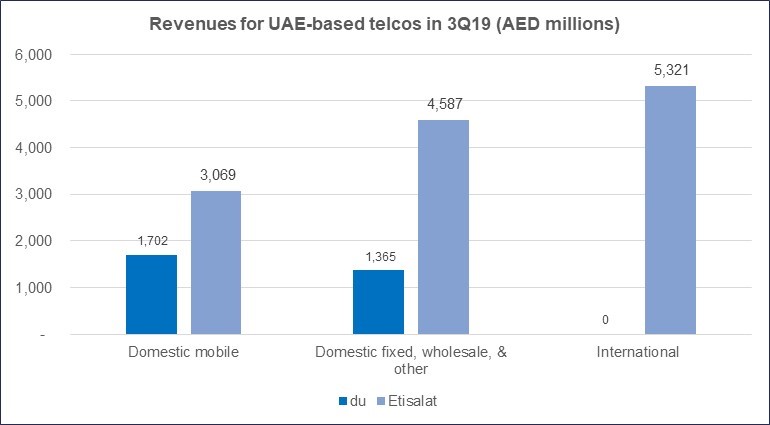

Etisalat and du are the only two telecom network operators in the UAE. The UAE government owns large ownership stakes in both operators, and limits competition in the sector. The creation of du in 2007 added a second competitor to the mobile market, but fixed line competition only began in 2015. At the end of September 2019, Etisalat has 10.54 million while du has 7.736 million mobile subscribers. Thus, UAE has about 186% mobile penetration rate, one of the highest in the world. UAE has also the highest smartphone adoption rate in the MENA region, and second only to Singapore, with smartphones accounting for 85% of total connections in Q2 2018.

Figure 2 shows the growth of the UAE’s population and mobile subscriber base from 2000-18.

Figure 2

Sources: IMF and ITU

The MVNO phenomena was started in 2017 with the launch of Virgin Mobile by du, which was immediately followed by Etisalat’s Swyp. These Mobile Virtual Network Operators are targeting the younger tech-savvy generation. The packages offered by these MVNOs are tailored more towards mobile data rather than phone calls and SMS services.

Etisalat and du have extensively deployed optical fiber throughout the country. FTTH (fiber to the home) service is also widely available in UAE. Based on September 2018 stats from the FTTH Council MENA, the UAE ranked number one (globally) with a 95.7% FTTH penetration rate. A small geography and a high average income both facilitate this. While competition in fixed line is only a few years old, du has built up a noticeable market share.

Figure 3 below illustrates revenues for the two companies by type, in 3Q19.

Figure 3

Source: company earnings reports

5G

Etisalat awarded contracts to both Huawei and Ericsson for the rollout of its 5G mobile network in February 2019. It plans to deploy 900 5G-enabled base station sites during 2019-20. Etisalat’s rival du plans to deploy 700 5G base stations during the same time frame. Huawei and Nokia are du’s 5G network suppliers. ZTE’s Axon 10 Pro 5G is one of the first 5G handsets (if not the first) that was launched by both operators in the UAE.

Connectivity

The UAE has two key landing stations for connectivity with international submarine cables. The Fiber-Optic Link Around the Globe (FLAG), South East Asia-Middle-East-Western Europe 3 (SEA ME WE 3), SEA-ME-WE 4 and Asia-Africa-Europe-1 (AAE-1) lands at the port of Fujairah, whereas SEA-ME-WE 5 lands at Kalba.

UAE also uses satellite earth stations such as 3 Intelsat (1 Atlantic Ocean and 2 Indian Ocean), 1 Arabsat, etc., for connectivity.

Spectrum

In November 2018, the regulator TRA issued 100 MHz to each of the two incumbent operators in the 3.3 to 3.8 GHz frequency range to offer 5G services. This free issuance of spectrum is hugely beneficial for operators’ financial health and network rollout.

In addition to this C-band assignment, the regulator is also looking at the 1427 MHz-1518 MHz, 24.25 GHz – 27.5 GHz and bands above 40 GHz for 5G. Both Etisalat and du also have spectrum assignments in 800, 900, 1800 and 2100 MHz bands to offer 2G, 3G and 4G services. Etisalat additionally uses the 2600 MHz band to provide 4G LTE service.

Key Challenges

The UAE’s key challenge is the commercialization aspect of 5G in conjunction with the heavy baggage of 2G, 3G and 4G networks.

UAE is one of the richest countries of the world with a GDP per capita of over $40K. The IMF expects the UAE economy to grow at 1.6% in 2019 and 2.5% per year through 2025. In the telecom sector, the duopoly and state-controlled structure has landed the operators in a reasonable financial state. With little possibility of a third player, the two operators as compared to many other markets have few things to worry about, at least in the near term.

Recommendations

To further streamline the process of effective and meaningful commercialization of 5G, the following steps may be considered:

3G Shutdown: TRA and operators may come up with a near term deadline to close down the 3G networks. The slower and less spectrally efficient 3G is definitely not required when better 4G and 5G networks are available. The 2100 MHz band which is used to operate 3G is not primarily used for 4G and 5G worldwide and thus keeping it for future use may not be worthwhile. Eventually, it will free up capacity, reduce the number of network elements and further improve their networks’ quality of service and overall financial health. Transition issues such as QoS degradation and vendor contract renegotiation are manageable.

2G Shutdown: The operators also have a huge customer base of low ARPU, price sensitive customers. The vast majority of these customers are expats (immigrants) and a large number of them have come from a poor and less educated background. With high tendency to save money for families in their home countries, cheaper 2G/3G phones are preferred over more tech-savvy and high-end devices. Regulators and operators should jointly consider developing a detailed roadmap for the discontinuation of 2G services. The roadmap may look into such issues as: the availability of low cost 4G and 5G phones, as most of the available low-end phones are not capable of operating on 4G/5G networks; reengineering of the required section of the networks including disposal of unnecessary elements; and, creation of awareness programs. Furthermore, 2G primarily operates in the 900 MHz band which has not been recommended for 4G and 5G.

5G Device Cost: Operators may further increase their due diligence with the device suppliers to lower the cost of 5G devices to attract masses. The current cost of a 5G device in UAE hovers around USD 800-1,200 as compared to $10-$30 for 2G/3G phones.

Vertical Markets: It will be difficult to have a good return on 5G investments without its enablement in vertical industries. An effective roadmap is needed to strengthen 5G in IoT (Internet of Things), AI (Artificial Intelligence), V2X (vehicle to everything – connected cars), etc., markets. The list of stakeholders is long and with perhaps many open as well as clandestine political agendas, it won’t be easy to come up with such a roadmap. The seven emirates and ministries / regulators along with the corresponding industries (education, finance, health, maritime, telecommunication, tourism, transportation, etc.) will eventually face an uphill battle.

New Entrants: With 5G and its enormous possibilities in vertical industries, the regulator (TRA) may conduct another round of due diligence on the viability of new entrants in the telecom space.

Thailand is making good progress in its goal of launching commercial 5G service in 2020. The recent auction of frequencies in the 700 MHz band, the agreements between operators and telecom equipment suppliers, as well the development in academia and 5G lab setups by suppliers in the Eastern Economic Corridor (at Chonburi) are all great steps in the right direction.

Recommendations

To further streamline the process of effective and meaningful commercialization of 5G following recommendations may be considered by the administration and operators:

• Provide a deadline to shutdown 3G networks. Operators should study this subject and deduce plans; • Consider further lowering the USO (Universal Service Obligation) contribution rate for the operators; • Execute effective field trials to understand the coexistence of satellite and IMT (International Mobile Telecommunication) in the C-band (3.4 GHz -3.7 GHz); • Auction either 26 GHz or 28 GHz but not both in the year 2020; • Do not consider the 2600 MHz for 5G in the near future as it will be difficult to achieve economies of scale, since it is not one of the desired bands for 5G at the world stage; • Recommend a footnote for the future use of 3.4-4.2 GHz for IMT at the World Radiocommunication Conference 2019; • Provide a 3 to 5 year frequency spectrum roadmap.

Thailand overview

The Kingdom of Thailand is a country at the center of the Southeast Asian Indochinese peninsula composed of 76 provinces. Home to over 69 million people, it shares borders with Cambodia, Malaysia, Myanmar and Laos. It also has a long coastline along the Gulf of Thailand (1,875 km) and the Andaman Sea (740 km), excluding the coastlines of some 400 islands (Figure 1). GDP per capita was $7,274 in 2018.

The Ministry of Digital Economy and Society was formed on October 03, 2002. It is responsible for national policy on digital development, statistics and meteorology. It is also responsible for managing country’s telecommunication networks and regulating cyber security. It manages two public telecommunication companies namely TOT (Telephone Organization of Thailand) Public Company Ltd and CAT (Communications Authority of Thailand) Telecom Public Company Ltd. Prior to the 2002 creation of the MDES, Thailand’s telecom sector was overseen by a Ministry of Information and Communication Technology.

The National Broadcasting and Telecommunications Commission or NBTC is the national and independent regulator in Thailand that manages both telecommunications and broadcasting sectors. It has the authority to assign frequency spectrum and regulate the two sectors in accordance with the Act on Spectrum Allocation Authority, Regulatory & Control over Radio & TV Broadcast and Telecommunications of 2010 (or NRA Act of 2010).

Mobile Operators

Thailand is a market of approximately 94 million mobile subscribers (June 2019), resulting in a mobile phone penetration rate of about 136%. It is predominantly a prepaid market having more than 70% share.

The mobile phone operators can be divided into two groups – stated owned enterprises and private companies. TOT and CAT are the state-run operators having a combined market share of around 2%. While their services share is tiny, TOT and CAT play important roles as concession holders for private telcos. In addition, their networks include lots of fiber in the backbone and backhaul, as well as cell towers, so they are important infrastructure suppliers to the private sector.

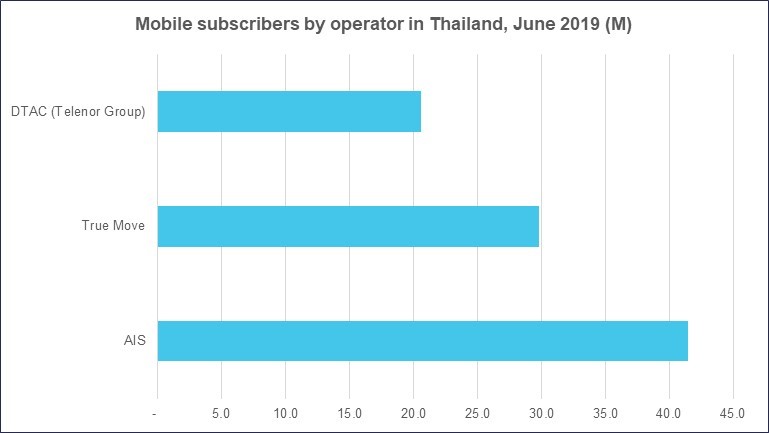

The key private telcos are three players – AIS (Advanced Info Service), TrueMove H and DTAC (Total Access Communication). AIS is the market leader with 41.5 million subscribers followed by True Move with 29.8 million. DTAC, which is owned by Telenor Group, comes in at number three with 20.6 million of users at end of June 2019 (Figure 2).

Figure 2

Source: company earnings reports

A number of MVNOs (Mobile Virtual Network Operators) are also present that provide services to their customers using the networks of the state-run enterprises. For example, Buzzme uses TOT’s network whereas Real Move depends on CAT’s network. These MVNOs lack their own radio frequencies and networks, instead they lease capacity from the two state run enterprises.

Fixed line Operators

Thailand’s fixed line subscriptions continue to decline as in other ASEAN countries due to heavy penetration of mobile phones and mobile broadband. The subscription total is down from 3.466 million in 2017 to 2.929 million in 2018. After the dissolution of TT&T (Thai Telephone & Telecommunications) in 2017, TOT took over TT&T’s operations. Now, TOT and AIS are the only two large fixed line operators remaining in the country. TOT has around 70% of the market while most of the rest belongs to AIS. The AIS fixed line customer base comes partly from its 2017 acquisition of CSLoxinfo (see “Running Converged Networks is Costly; A View From Thailand”). In addition to AIS there are several smaller ISPs with fiber and/or DSL networks, some targeting mainly consumer (such as 3BB, owned by Jasmine) and some focused on enterprise (such as Symphony).

Spectrum

Over the last few years the regulator conducted multiple auctions for the launch and promotion of 3G/4G services. The most important one happened in 2012, when the regulator allocated 45 MHz in the 2100 MHz frequency band. An assignment of 15 MHz was made to each of the three mobile phone operators. This spectrum is currently used to offer 3G/4G services. To keep up with the pace of demands from 3G/4G networks, the regulator successfully managed to auction some spectrum in the 900 MHz and 1800 MHz frequency bands in 2015.

To kickoff 5G, the regulator conducted an auction of 700 MHz in June 2019. A block of 2 x 10 MHz was assigned to each of the three private operators and the respective licenses will be valid for the next 15 years starting from October 01, 2020. The auction was conducted at a reserve price of THB17.6 billion ($562 million) per block. This frequency band could be instrumental in kicking off 5G in the country.

The current spectrum assignments for each operator is are shown in Table 1.

Thailand is moving ahead to launch 5G during 2020.

The regulator (NBTC) took a great step in December 2018 by mandating operators to shut down 2G services by October 2019 in order to free up capacity for 5G services. The recently concluded 700 MHz auction, along with the existing bands that were in use for 2G services, will also help in the launch and development of 5G.

There are other positive signs:

Vendor deals: The recent agreements of Nokia, Huawei and ZTE with AIS on the development of 5G use cases for a wide range of industrial verticals.

5G use case development: besides spectrum auctions, NBTC is also facilitating the development of 5G at leading educational institutes in each region. After an initial trial at Chulalongkorn University, 5G service was launched at Chiang Mai University (CMU), Khon Kaen University (KKU) and Prince of Songkla University in the 25 and 28 GHz bands. CMU is situated in northern Thailand, KKU in northeast, PSU in south whereas Chulalongkorn University is located in Bangkok (central Thailand). This project will assist academia as well the telecom sector in the development of 5G across the length and breadth of Thailand.

R&D: Another key development is the 5G lab setups by Huawei, Nokia and Ericsson. These are located in Chonburi, about 90 km (56 miles) southeast of Bangkok. The surrounding area is the target of the Eastern Economic Corridor, which Thailand is hoping to develop by attracting $45B of new investment.

Connectivity

Thailand’s domestic fiber optic cable network spanned 310,000 kilometers at the end of 2018. Most of this is owned by the public sector (210,000 kilometers in total), in particular TOT and CAT. The private sector owns the remaining 100,000 kilometers.

Thailand has multiple submarine cable landing stations for international connectivity. The main submarine cables landing in Thailand are SEA-ME-WE 3, SEA-ME-WE 4, Thailand-Indonesia-Singapore cable, Asia-Pacific Cable Network, Thailand-Vietnam-Hong Kong cable, and FLAG (Fiber-Optic Link Around the Globe). In addition, a new cable system, the SJC2 (South-East Asia Japan Cable System 2) cable is under construction and will land in Songkhla by end of next year.

Key Challenges

Thailand is in a reasonable position to launch 5G. However, there are still a number of challenges that need to be addressed:

The famous C-band: Frequencies in the range of 3.4 to 4.2 GHz, which is part of the core 5G band, are extensively used for TV broadcasting services in Thailand. This spectrum won’t free up for a while. Even though the only satellite that operates in 3.4 GHz to 3.7 GHz range is Thaicom5, its license will not expire before 2022-23. The newer Thaicom6 is also an issue, as it operates in the 3.7-4.2 GHz range and has a valid license till 2029. Field trials are underway in Thailand to understand the compatibility / co-existence of IMT with existing satellite services in the 3.4 to 3.7 GHz band. The only possibility at least for the near future is 3.3-3.4 GHz band for 5G services.

Spectrum Roadmap: lack of a clear spectrum roadmap remains an issue in Thailand. It’s promising that, in addition to the recent 700 MHz auction, NBTC is planning to auction 2.6 GHz, 26 GHz, 28 GHz bands in 2020. However, the cost of acquisition issue needs to be addressed.

Recommendations

To further streamline the process of effective and meaningful commercialization of 5G, the following steps may be considered:

3G Shutdown: Operators should start thinking about shutting down their 3G networks. This will free up capacity, reduce the number of network elements, reduce their annual license cost, and spectrum can be returned to the regulator if needed and/or possible or can be reused for 5G if possible. In a nutshell, it will improve their networks’ quality of service and overall financial health. Transition issues such as QoS degradation and vendor contract renegotiation are manageable.

USO Contribution: Operators make USO obligatory payments out of their revenues to the government. These payments are made to extend the reach of telecommunication services to underserved and remote areas of the country where getting a return on investment is next to impossible. Though the government has recently cut the USO fee to 2.5% from 3.75%, the rate is worth a relook.

2020 Spectrum Auction: A 2×10 MHz block in 700 MHz is not suitable to offer real 5G broadband services and thus additional frequencies are needed. Fortunately, there are other options. According to NBTC, a total of 190 MHz in 2.6 GHz, 2.25 GHz of bandwidth in the 26 GHz band, and 3 GHz in 28 GHz are available and all are expected to be put on auction in 2020. We recommend that either 26 GHz or 28 GHz band may be auctioned but not both in 2020. Secondly, we suggest that 2600 MHz may not be put for auction as it is not one of the desired bands at the world stage for 5G in 2020:

Both bands (26 GHz and 28 GHz) have enough bandwidth to offer 5G for the coming years

Not to give additional financial burden to the operators

C-band (3.4 GHz – 3.7 GHz): A quick completion of the currently underway 5G and satellite co-existence/ compatibility trial will be good omen, particularly if the results are positive. Thailand may recommend a footnote for the future use of 3.4-4.2 GHz for IMT at the World Radiocommunication Conference 2019.

3.3 GHz – 3.4 GHz: This range may only be made available if existing satellite usage in 3.4 – 3.7 GHz can co-exist with IMT, otherwise bandwidth is not enough to be shared among three operators along with the guard band of 10-20 MHz.

Spectrum Roadmap: A clear 3 to 5 year roadmap is needed to assist operators and their shareholders in their decision-making process.

Indonesia, the world’s fourth most populous country, is expected to face an uphill battle to enable 5G. Reasons include its complex geography, unavailability of core 5G frequency band (i.e. C-band 3.3 to 4.2 GHz), and dwindling operator revenues. The goal of this post is to briefly address these challenges and make suggestions for how to improve 5G’s outlook in the country.

Recommendations

There are several steps that would improve the outlook for 5G in Indonesia. The Ministry of Communication and Informatics (MCI) may:

• take steps to make the 3.3-3.4 GHz band available for International Mobile Telecommunication (IMT);

• recommend a footnote for the future use of 3.4-4.2 GHz for IMT at the World Radiocommunication Conference 2019;

• conduct effective spectrum auctions for suitable millimeter wave band(s), perhaps starting with 28 GHz; and,

• remove roadblocks to ease the process of cellular market consolidation.

Meanwhile Indonesia’s operators should utilize the connectivity provided by the recently completed Palapa Ring project to expand their business in remote areas, and work with MCI for an effective market consolidation.

Indonesia overview

Indonesia, home to over 271 million people, is an island country in Southeast Asia comprised of more than 17,000 islands. It is the world’s 4th most populated country with the world’s 16th largest economy in terms of nominal GDP (gross domestic product).

Indonesia shares land borders with Papua New Guinea, Timor Leste, and the eastern part of Malaysia. Australia, India, Palau, Philippines, Singapore, Thailand, and Vietnam are its maritime neighbors (Figure 1).

Indonesia’s Ministry of Communication and Informatics is responsible for organizing government policy in the field of Information and Communications Technology. In 2003, the Ministry established the Indonesian Telecommunications Regulatory Body (BRTI) to which it delegates authority to regulate, supervise and control telecommunications networks and services. BRTI is also responsible for executing frequency spectrum auctions.

Mobile operators

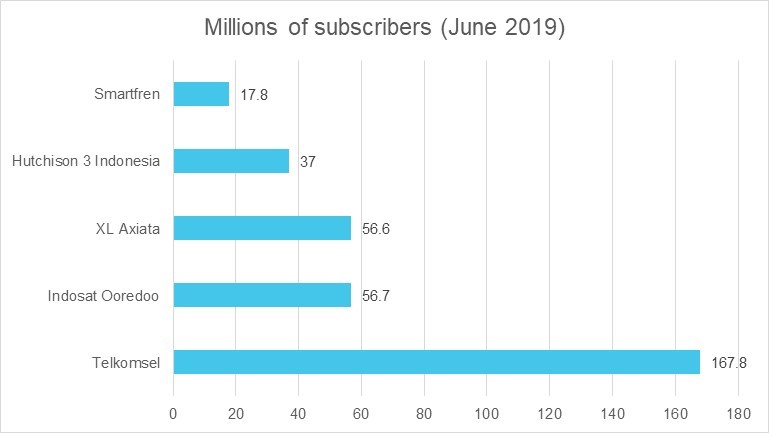

Indonesia is the fourth largest cellular market in the world with more than 330 million subscribers. The market is dominated by five cellular players, including state-owned Telkomsel and privately held Indosat Ooredoo, Hutchison 3 Indonesia, XL Axiata, and Smartfren. (Figure 2) SingTel has a 35% stake in Telkomsel, with the remainder held by incumbent Telkom Indonesia.

2G (GSM/GPRS) is still the dominant technology with close to 45% of subscriptions. Mobile broadband comprised of 3G and 4G networks has made substantial progress since inception. Operators continue to expand 4G network coverage to remote areas. For example, Telkomsel deployed 22,000 4G LTE base stations in its network between January and September of 2019, stretching deeper into rural regions.

Figure 2: Mobile subscriber totals for Indonesian telcos, June 2019 (millions)

Source: Company earnings announcements

Although 5G is making headlines globally, Indonesia’s operators are not in a rush to deploy as they continue to expand 4G penetration and await a settlement between the US government and Chinese vendors, and perhaps for market consolidation.

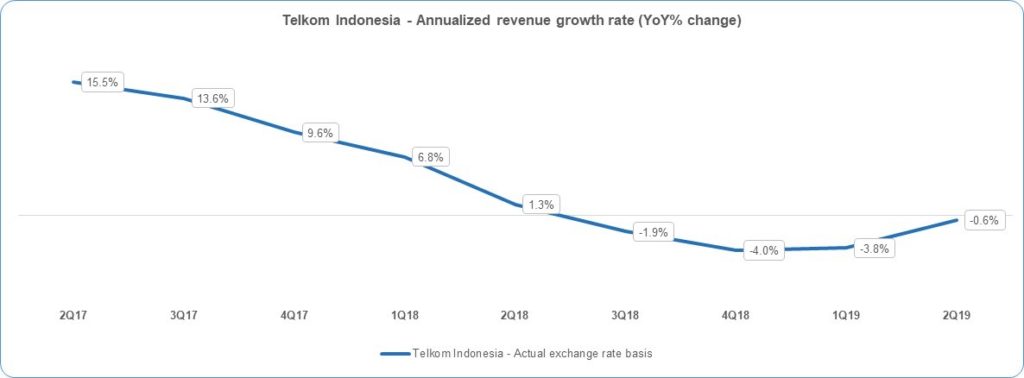

The Ministry is in favor of consolidation due to declining financial health of the operators. As in most countries, telcos in Indonesia are not finding topline growth easy to achieve. Market leader Telkom Indonesia, for instance, has faced negative revenue growth rates over the last few quarters, in USD terms (Figure 3).

Figure 3: Annualized revenue growth rate for Telkom Indonesia (YoY % change), USD-basis

Source: MTN Consulting

If measured in local currency, Telkom’s revenue growth rates are slightly better than the above figure. A weakening currency has worsened the comparisons. Currency issues have also made imported network equipment more expensive recently, a big issue in Indonesia where capex to revenue ratios are often well above 20%.

Independent tower operators

To help cope with high network costs, operators in Indonesia have transferred the bulk of their radio tower business to third parties (tower companies). Indonesia’s five big tower companies ended June 2019 with control of 45.3K towers, up from 42.5K in June 2018. Tower spinoffs continue. For example, Indosat Ooredoo recently agreed to sell as many as 3,100 telecommunication towers to local tower providers. PT Daya partner Telekomunikasi (Mitratel) will buy 2,100 of Indosat’s towers while PT Professional Telekomunikasi Indonesia (Protelindo) will acquire 1,000 with a total transaction value of about US$456 million.

This asset restructuring has helped Indonesian telcos lower their cost base and accelerate service coverage. It has also created a viable new industry of asset specialists, classified by MTN Consulting in its global research as “carrier-neutral network operators” (CNNOs). The largest of the group, Sarana Menara Nusantara, had total 2018 revenues of $412M, about 4% of the $9.2B booked by the largest local telco, Telkom Indonesia.

Spectrum

In 2015, the Ministry allocated an additional 246 MHz of radio frequency spectrum for mobile broadband purposes. The target allocation is 350 MHz according to the Ministry’s 2015-2019 Strategic Plan. These spectrum assignments have been made through various methods including auction, refarming, reallocation, etc. Indonesia’s mobile service providers are operating in various bands now, including 450, 800, 900, 1800, 2100 and 2300 MHz (Table 1).

Table 1: Operating frequency and bandwidth allotted (MHz)

Company

450

800

900

1800

2100

2300

Total

H3I

20

30

50

Indosat

25

40

30

95

STI

15

15

Smartfren

22

22

Smarttel

30

30

Telkomsel

30

45

30

30

135

XL Axiata

15

45

30

90

Total bandwidth

15

22

70

150

120

60

437

Source: “Analysis of 5G Band Candidates for Initial Deployment in Indonesia,” 2018, by Septi Andi Ekawibowo, Muhammad Putra Pamungkas, and Rifqy Hakimi of the Bandung Institute of Technology (page 3)

Note: PT Sampoerna Telekomunikasi Indonesia (STI, or “Net1”) is a regional operator which started operations in 2018. It utilizes the 450 MHz frequency band to offer 4G LTE.

While the Ministry hasn’t explicitly addressed spectrum allocations suitable for 5G, it is trying to free up spectrum. For instance: digitalization of television broadcasting: The ministry is taking steps to free up spectrum by switching off analog broadcasting in consultation with other stakeholders.

Fixed line

The fixed-line segment is quite small as compared to wireless telephony market due to complex national geography, high up-front cost and operational expenses. The state-owned Telekom has the monopoly in this segment, while Indosat is the second major player, both providing services mainly in the urban areas. There are a number of alternative broadband providers and ISPs which also invest in network infrastructure locally.

Vendors

Chinese suppliers are stronger than usual in Indonesia, but Huawei, ZTE, Ericsson and Nokia all have significant shares of the local network infrastructure market. That includes 4G, and will likely extend to 5G. Just recently, ZTE signed a Memorandum of Understanding (MoU) with Telkom to deploy 5G, while Nokia executed the first 5G millimeter wave network trial with Hutchison 3 Indonesia.

Geographic challenges

Development of infrastructure to provide ICT (Information and Communications Technology) services including broadband is a unique challenge due to Indonesia’s complex geography consisting of many remote islands and rural regions. Land-based connectivity is cumbersome due to oceanic separation between islands and between smaller islands to major cities, which are in some cases 1,000s of miles away. For example, the distance between Jakarta (capital of Indonesia) and Kupang (capital and major port of Indonesian province of East Nusa Tenggara), is 1,023 nautical miles. Thus, in many cases the preferred methods to provide connectivity include satellites, microwave radios and submarine fiber optic cable.

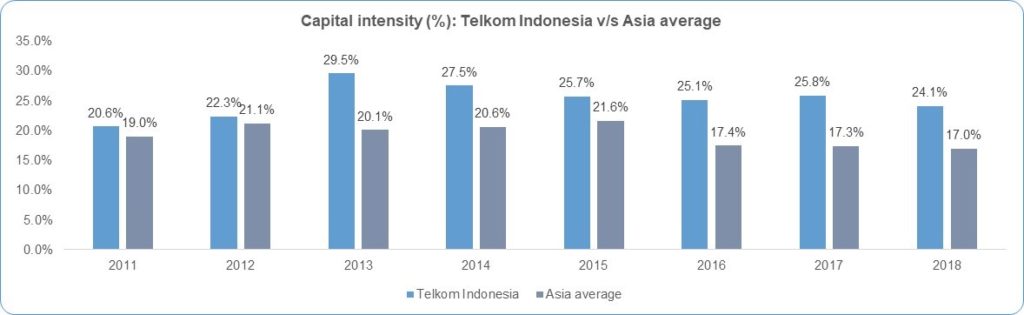

Due in part to its geography and disperse population, operators require higher capital investments than many other markets. For example, the capital spending of Telkom Indonesia has been higher than the Asia average consistently since 2011 (Figure 4).

Figure 4: Telkom Indonesia capex/revenues vs. Asia average, 2011-18

Source: MTN Consulting

Satellite-based Communications: Indonesia launched its own domestic satellite system in mid-1970s. The largest segment of the satellite telecom market is the backhaul connectivity followed by Internet communications for the consumers. However, only a small portion of total traffic is carried over the satellites.

Submarine Cable based Communications: Indonesia is lagging behind to some extent when it comes to providing international connectivity through submarine cables. Recent investments in new cables will help. For example, the SEA-ME-WE 3 (South East Asia – Middle East – Western Europe 3) lands in the Indonesian cities of Jakarta and Medan. Connectivity has been further improved with SEA-ME-WE 5, which was inaugurated in 2017. The SEA-ME-WE 5 cable lands in the Indonesian cities of Medan and Dumai. A number of other smaller cables connect the Indonesian market to Australia, Malaysia, Singapore and Thailand. New projects like INDIGO and the Australia-Singapore cable will help Indonesia as well.

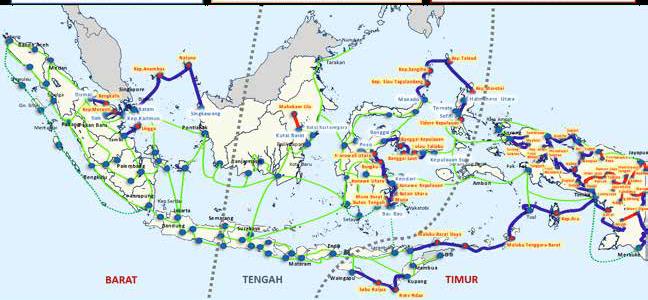

Palapa Ring Project

The Ministry has taken multiple large-scale infrastructure development projects to overcome the digital divide. One key project is the Palapa Ring network, a new national backbone network utilizing a mix of submarine and terrestrial routes. Completed in October 2019, this project took several years and $1.3B to complete. This new fiber optic backbone can be used by operators to provide broadband services. Figure 5 illustrates the Palapa project, using blue lines for fiber and blue dots for optical nodes.

Indonesia was ranked 111th out of 176 countries in the ITU’s 2017 ICT Development Index. This index measures the levels of economics, prosperity, literacy and other skills that enable citizens to take full advantage of ICTs. Much can be done to improve the ICT status of Indonesia, and telecommunications has a role to play.

5G could be one of the key enablers to improve the ICT standing of the country. To enable 5G, though, Indonesia at least needs a long-term roadmap, a solid fiber optic cable network, effective frequency spectrum auction(s) and a strategy for market consolidation.

The development of some of the pieces of this puzzle are still in the rudimentary stage and more concrete steps are needed. Our recommendations for further progress are as follows:

Long-term policy roadmap: Indonesia’s telecom Ministry (MCI) may need a long term roadmap for development of the sector, with three prongs. One to solve the technicalities (e.g. spectrum allocation); another to ensure an opportunity for effective return on investment; and thirdly and most importantly its benefits and implications for the people of Indonesia. With strong policy coordination, the government can use 5G as an enabler to reduce the broadband connectivity gap between its rich and poorest regions, create jobs and strengthen its ICT standing in the world.

Market Consolidation: Many successful markets have 3 to 4 cellular providers; Indonesia has five operators. Consolidation should help strengthen the dwindling financial strength of these companies. Out of the five operators, only Telkomsel has an EBITDA of 50 percent whereas Indosat, XL Axiata and Smartfren all suffered losses in 2018.

Frequency Spectrum: in Indonesia, the 5G core spectrum band of 3.5 GHz (i.e. 3.3 – 3.8 GHz) and frequencies up to 4.2 GHz are currently used for fixed satellite service (FSS) applications. FSS applications include tv broadcasting, banking communications, and Internet connectivity. In more granular terms, the range from 3.3 to 3.4 GHz is used for fixed wireless broadband and rest for FSS. FSS is extensively used in this particular band and thus to use this band for 5G will be a daunting task. Indonesia may reflect its intention for the future use of this band for mobile and more specifically for IMT (International Mobile Telecommunication) in the footnotes in the coming WRC-19.

As the availability of the core band is next to impossible in the near future, it is important to pay more attention to millimeter wave band frequencies. The recent completion of the live 5G trial in 28 GHz using Nokia’s equipment on Hutchison 3 Indonesia network is a good step. Along similar lines, ZTE and Smartfren have also conducted an indoor 5G trial on 28 GHz.

Spectrum Auctions: Spectrum auctions for 5G particularly for the core band need to be executed by keeping a strong balance between the wish-list of the government and desires of the operators. There is no magic figure for the base price of a particular frequency band, which depends on a number of variables. However, it should be lower for millimeter wave bands as compared to the core band due to much higher implementation costs of the former.

Connectivity: A solid transport network including backhaul is a must for the success of broadband and 5G. The Palapa Ring project and ongoing investments by local CNNOs and telcos will both boost the development and implementation of 5G.

–

*Saad Asif is a Contributing Analyst for MTN Consulting and a recognized industry expert in wireless communications. He has worked in the field of telecommunication for over 21 years, and has authored three books and multiple peer-reviewed technical papers. Saad has been granted multiple patents and is a senior member of the IEEE.

Optimistic 5G forecasts assume that telcos’ spectrum needs are met

Ericsson recently predicted that by 2024 5G subscriptions will reach 1.9 billion, 35 percent of traffic will be carried by 5G networks and up to 65 percent of the global population could be covered by 5G. This is one of the many forecasts that predict the success of 5G, however there are many variables attached to it. A key one is the availability of suitable, affordable and importantly harmonized radio frequency spectrum, which is the focus of this blog.

Harmonized spectrum is key for 5G success

At the upcoming World Radiocommunication Conference (WRC), the overall goal of the telecommunication world at is to secure a sizeable chunk of harmonized spectrum for 5G.

Spectrum harmonization drives economies of scale, better battery life (as phones don’t need multiple radio modules and to toggle between frequencies), less cumbersome roaming and lesser cross border interference. It’s essential for 5G to succeed.

Government policymakers want to auction or license this harmonized spectrum to cover their current and future budgets. Telecom network operators on the other hand are interested in getting this harmonized band(s) at a reasonable cost from governments in order to meet operational excellence requirements and achieve their business targets in partnership with their vendors.

Background on spectrum

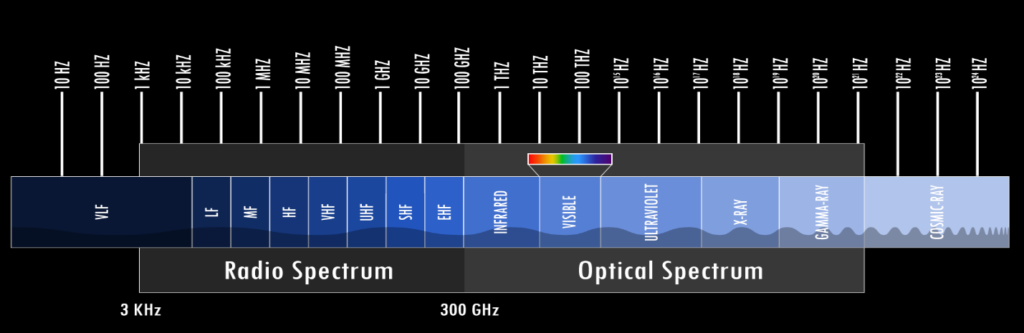

Wireless communications require airwaves to provide services. Airwaves, or electromagnetic spectrum, consist of a range of all types of electromagnetic radiation, from radio waves to gamma rays. The range of frequencies that are used for providing mobile and WiFi connectivity falls under the radio frequency (RF) portion of the electromagnetic spectrum. RF spectrum ranges from 3 kHz to 300 GHz (Figure 1).

Figure 1: Range of frequencies in wireless communications

Source: Nasa (https://imagine.gsfc.nasa.gov/science/toolbox/emspectrum1.html)

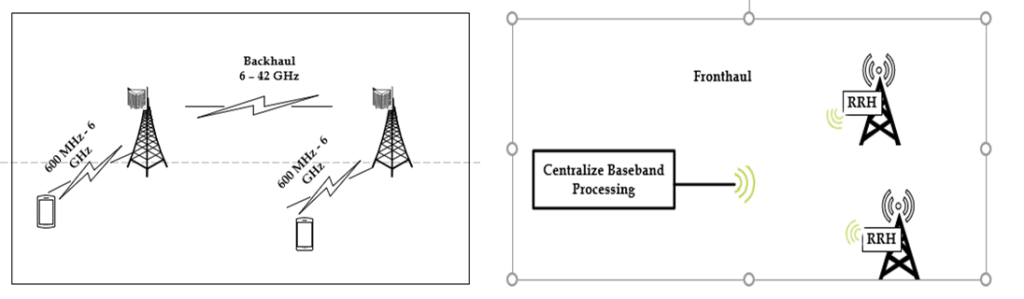

Mobile communications – a subset of wireless communications – primarily takes place in the range of 600 MHz to 42 GHz. The lower frequency bands are suitable for addressing communications between mobile phones and base stations (radio towers) while the high bands are used for supporting backhaul connectivity between radio towers. Fronthaul, which is a much newer concept, connects remote radio heads mounted on towers to baseband units located in a centralized location. Fronthaul requires much higher bandwidth and minimal latency and thus for the most part it is supported with optical fiber. However, in case fiber is not available, a wireless medium can be used (e.g. microwave). (Figure 2).

Figure 2: Use of radio waves in cellular networks

Source: MTN Consulting

The electromagnetic spectrum requires proper management, allocation, assignment and harmonization at a global level. That’s because wireless communications isn’t limited by national boundaries, and a global approach helps facilitate economies of scale. This huge function is performed by the ITU (International Telecommunication Union), which is the United Nations’ specialized agency covering information and communication technologies (ICTs). More specifically, the ITU’s Radiocommunication sector (ITU-R) takes care of this obligation at the global level.

ITU-R allocates spectrum through the pivotal World Radiocommunication Conference (WRC), which takes place once every 3-4 years. WRC is the most significant inter-governmental event related to the frequency spectrum. WRC has a mandate to review, and, if necessary, revise global Radio Regulations, the international treaty governing the use of the radio-frequency spectrum and the geostationary-satellite and non-geostationary-satellite orbits. This treaty is the basis for the harmonization of spectrum worldwide.

WRC allocates frequencies to everything that needs airwaves for execution – from as small as garage door openers all the way to space satellites, and everything in between (terrestrial, aviation, maritime, etc.).

Once spectrum is allocated at the WRC, national regulatory bodies such as the FCC and can assign specific bands to specific service providers (such as AT&T, Sprint, etc.) through a license for a specific number of years.

To predict the future, you have to understand the past

The focus of this blog is three-fold: (a) to provide a brief summary of the key activities that took place at WRC-15 (b) to give a sneak preview of the upcoming WRC-19 and (c) to analyze the cost and global implications of spectrum for 5G.

Recap from WRC-15

The demand for wireless connectivity and applications on the go is continuously on the rise. The wireless industry requires quick access to frequency spectrum and a lot of it, on a worldwide basis. Back in 2014, the ITU-R predicted that the world would need an additional 1340-1960 MHz for broadband services by 2020. The aim of the world body was to get harmonized spectrum in the range suggested by ITU-R, preferably on a global scale, if not then at least to some extent on the regional basis.

To keep the story short, WRC-15 can be considered as the first major international event that looked into allocating frequency spectrum for 5G. However due to some geopolitical challenges and presence of many existing services, the WRC-15 was only able to allocate 51 MHz for IMT (International Mobile Telecommunications) systems on the worldwide basis. In addition to this 51 MHz allocation which was made in the L-band (1-2 GHz), sizeable additional allocations were made on a regional basis. The total allocation was over 1500 MHz, satisfying the regional requirements for the most part (Table 1).

To clarify, IMT is the flagship project of the ITU-R and covers 3G, 4G and 5G systems. The ITU-R doesn’t allocate spectrum for a specific mobile generation but rather in generic terms of MOBILE and IMT. This capitalization means that the service has been allocated on a primary basis and no other service can interfere in its operations.

In the past, the identification of spectrum as MOBILE for cellular/broadband systems (including 2G) was sufficient. However, the advent of 4G/5G has the brought the concept of IMT systems to the limelight and now even if a service is already allocated for MOBILE, it doesn’t necessarily mean that it can be used for it unless it has been identified as IMT in the footnotes.

Table 1: IMT allocation at WRC-15

Band (MHz)

Regions (or parts thereof) *

Bandwidth (MHz)

450-470

2

20

470-698

2 & 3

228

694/698-960

1, 2 & 3 (not worldwide)

262

1427-1452

Worldwide

25

1452-1492

2 & 3

40

1492-1518

Worldwide

26

1710-2025

2

315

2110-2200

2

90

2300-2400

2

100

2500-2690

2

190

3300-3400

1, 2 & 3 (not worldwide)

100

3400-3600

1, 2 & 3 (not worldwide)

200

3600-3700

2

100

4800-4990

2 & 3

190

Sources: 5G Mobile Communications: Concepts and Technologies, and the ITU. *Region 1 comprises of Europe, Africa, the former Soviet Union, Mongolia, and the Middle East west of the Persian Gulf, including Iraq. Region 2 includes Americas including Greenland, and some of the eastern Pacific Islands. Region 3 covers non-FSU (former Soviet Union) east of and including Iran, and most of Oceania.

WRC-15 also identified several bands as study items for their potential usage for IMT. The range covers various bands from 24.25 GHz to 86 GHz. These bands are already providing a number of services particularly backhaul and satellite. The specific services in these bands also can differ by region to some degree. Therefore, spectrum sharing and compatibility studies were required to look at their applicability of co-existence with IMT.

WRC-19 Preview

Before diving into WRC-19 it is worthwhile to look into the work executed by 3GPP in this regard after WRC-15. 3GPP, the flagship organization for 4G and 5G specifications, identified the following two frequency ranges:

Frequency Range 1 (FR1): 410 MHz to 6000 MHz with channel bandwidths in the range of 5 to 100 MHz with increments of either 5 or 10 MHz. This frequency range is applicable for both frequency and time division multiplexing modes.

Frequency Range 2 (FR2): 24.25 GHz to 52.60 GHz with channel bandwidths of 50, 100, 200 and 400 MHz supporting operations only in time division multiplexing mode.

3GPP focuses more on the nitty gritty of spectrum which has been identified in broad terms by ITU-R. 3GPP works more on the lines of identifying channel bandwidths and duplexing modes to support the underlying mobile services.

In preparations for WRC-19, the ITU-R as per its practice executed the two Conference Preparatory Meeting (CPM) sessions. In February 2019, the ITU-R issued a close to 1,000-page “CPM 19-2” report, designed to assist in preparations for and deliberations at WRC-19. It can be said that hundreds of resources, thousands of workforce hours and millions of dollars have been spent to study the subject frequency range.

The upcoming WRC-19, scheduled to take place later this quarter, has two major tasks when it comes to the allocation for MOBILE/IMT.

First to conclude on the applicability of the identified bands for MOBILE / IMT as required by agenda item 1.13 (Table 2). The CPM 19-2 report forecasted that IMT will require 0.33 GHz to 12 GHz of spectrum in the ranges of 24.25-33.4 GHz, 37-52.6 GHz and 66-86 GHz, depending upon the metrics, assumptions and frequency range. The problem is that all the bands listed in Table 2 are already in use. Further identification for IMT on a primary basis could face stiff opposition particularly from the satellite community at the WRC-19. Opposition from satellite is even more an issue than 2015 as many new players have entered this space, including some deep-pocketed companies like Amazon and Facebook.

Table 2: Applicability of identified bands for MOBILE/IMT (WRC-19 conference prep, Agenda item 1.13)

Source: ITU (https://www.itu.int/dms_pub/itu-r/opb/act/R-ACT-WRC.12-2015-PDF-E.pdf, and https://www.itu.int/dms_pub/itu-r/opb/act/R-ACT-CPM-2019-PDF-E.pdf)

Second, WRC-19 will need to look into spectrum allocation issues affecting several other big markets as listed in agenda items 1.11, 1.12, 1.14 and 1.16 and their implications on existing and future IMT systems:

Railway radiocommunication systems between train and trackside within existing mobile service allocations – RSTT

Intelligent Transport Systems (ITS) under existing mobile-service allocations

High-altitude Platform Stations (HAPS), within existing fixed-service allocations, and

Radio local area networks (RLAN), in the frequency bands between 5.150 GHz and 5.925 GHz

A brief summary of the key bands under consideration for these services is provided in Table 3 below. There are several bands that are already in use for IMT and thus any allocation to any new service needs to be justified and obtain consensus from administrators.

Table 3: Key bands for RSST, ITS, HAPS & WLAN

Potential Service

Key Bands Under Consideration

RSST

138-174, 335.4-470, 703-748, 758-803, 873-925, 918-960, and 1770-1880 MHz; 43.5-45.592 GHz and 92-109.5 GHz

ITS

5850-5925 MHz

HAPS

6.44-6.52, 21.4-22, 24.25-27.5, 27.9-28.2, 31-31.3, 38-39.5, 47.2-47.5 and 47.9-48.2 GHz

RLAN

5150 – 5925 MHz

Source: MTN Consulting

Big battles lie ahead

At this stage, the telecom industry is not close to achieving its target of harmonized, adequate 5G spectrum resources. Basically, there are two camps – one is favored by China and other by the USA. Disagreements are not settled easily at this stage as there is a first mover advantage in the development of mobile wireless generations. The market leader can set the stage for future infrastructure development, product development and specifications. In this context, three ranges of spectrum bands have been considered namely:

• low band (sub 1 GHz) which is used heavily for broadcasting and wireless services.

• mid band (1 GHz to 6 GHz) which is primarily used for wireless services.

• millimeter wave or mmWave (24 GHz to 100 GHz) which is used for many non-mobile services (Table 2)

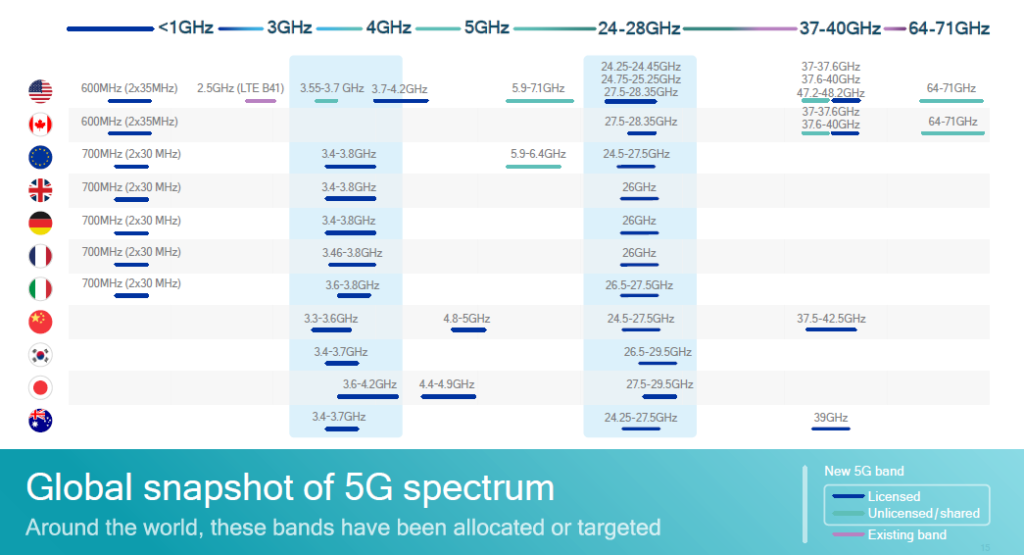

The battle hovers around the sub 6 GHz and mmWave bands. China is looking towards 3.5 GHz whereas the USA is focusing on multiple millimeter bands. The mid band, particularly the 3.5 GHz band that ranges from 3.3 to 3.8 GHz, is the most sought after band for use as a core band for 5G. That’s because of this band’s availability and lower deployment costs as compared to mmWave bands. China already assigned 200 MHz in this mid band. By contrast Japan and South Korea are working in both mid and mmWave bands. The rest of the world for the most part is playing catch-up on 5G spectrum assignments (Figure 3)

The US faces a unique problem in the mid-band. Namely, the US Department of Defense currently holds roughly 500 MHz in the 4 GHz range and thus it cannot be used for commercial operations. According to a DoD report, the estimated time required to clear spectrum (relocate existing users and systems to other parts of the spectrum) and then release it to the civil sector, either through auction, direct assignment, or other methods could take 10 years. Spectrum sharing between entities is another option and is a slightly faster process, but it could still take five years according to the same DoD report. Thus, the FCC has focused on the mmWave band. It had to auction out 24 GHz and 28 GHz bands and is planning to offer 37, 39 and 47 bands as well in the future. This is one of the key factors behind the limited coverage launches of 5G in USA. Verizon’s 5G network is based on the 28 GHz and 39 GHz bands, AT&T uses 39 GHz, and T-Mobile is planning 28 GHz. Sprint is eyeing the 2.5 GHz band as it doesn’t have any spectrum assets in the mmWave range.

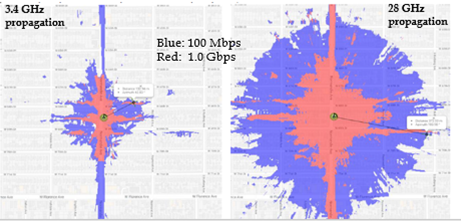

A study conducted by Google for DoD found severe limitations in the mmWave band. It concluded that for the same number of cell sites (macro cell sites and rooftops), 1 Gbps can only be provided to 3.9% coverage area at 28 GHz (US model) as compared to 21.2% at 3.4 GHz (Chinese model). The same study also estimated that it will require approximately 13 million utility pole-mounted 28-GHz base stations (one of the key choices of US operators for mmWave) and $400B in capex to deliver 100 Mbps edge rate at 28 GHz to 72% of the U.S. population, and up to 1 Gbps to approximately 55% of the U.S. population. Figure 4 illustrates the problem, showing the propagation difference between 28 GHz and 3.4 GHz deployments on the same pole height in a relatively flat part of Los Angeles.

Figure 4: Propagation difference in Los Angeles: 28GHz vs 3.4GHz

In a nutshell, mmWave bands will likely have a detrimental impact on operators’ budgets, at a time when they are not eager to ramp up capex. At the end of 2018, Verizon held ~$120B in debt with ~4% dividend yields, while AT&T held ~$175B in debt with over 6% dividend yields. T-Mobile holds ~$25B in debt, and Sprint holds ~$40B in debt. These companies are at the forefront of the U.S. effort to develop 5G, but their balance sheets suggest that they may struggle with the cost of a full mmWave network roll-out and the infrastructure it would require.

Conclusion

The wireless world’s technology leadership role will be at stake at WRC-19. History has proven that having access to the right set of spectrum assets can deliver a competitive advantage in the overall supply chain for years to come. The implications are vast both from the commercial and strategic point of views, impacting governments, operators, vendors, and ultimately jobs.

As of today, the industry lacks harmonized frequency bands for 5G. Perhaps at the end of WRC-19 the world will be closer to achieving this goal.

Stay tuned for more news from MTN Consulting on RF Spectrum and WRC-19!

–

*Saad Asif is a Contributing Analyst for MTN Consulting and a recognized industry expert in wireless communications. He has worked in the field of telecommunication for over 21 years, and has authored three books and multiple peer-reviewed technical papers. Saad has been granted multiple patents and is a senior member of the IEEE.

Huawei has dominated telecom news since the arrest last December of the Chinese vendor’s CFO in Vancouver. Since then, the US Commerce Department has restricted Huawei’s access to US-built tech components, including Google’s Android ecosystem. Huawei needs these components, so the heat is on. What happens next?

Let the Huawei chaos begin

Those waiting for a grand resolution to US-China disputes surrounding Huawei will be disappointed – the company’s problems did not arise with the Trump administration’s trade battles. Concerns about Huawei’s private company origins and independence from the Chinese state are fairly bipartisan in the US, at least two decades old, and shared by many European and Asian governments.

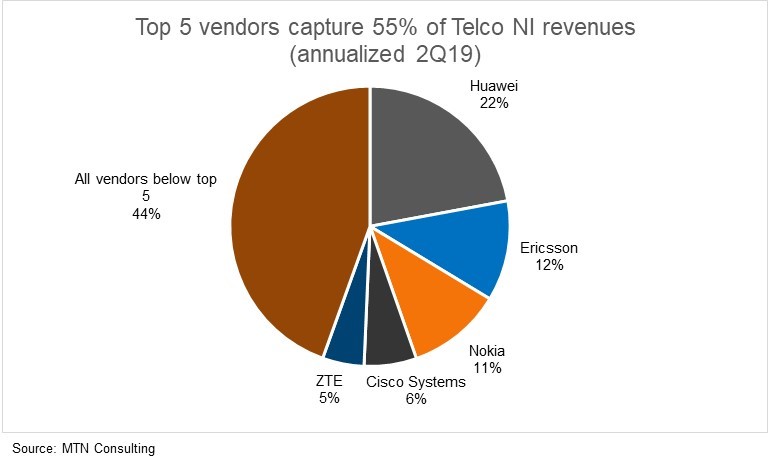

Yet Huawei certainly isn’t going anywhere; it has the broadest portfolio of products in the industry, and its 22% market share in network infrastructure sales to telcos (“Telco NI”) is nearly as much as Nokia and Ericsson combined (figure, below). Since Meng’s arrest, the vendor has hardly backed away from its ambitions – and the Chinese government has made clear its support for Huawei’s long term growth.

In the developing world, Huawei’s network infra share is over 30%, and its share in most developing markets is rising, due in part to “China Inc”. Huawei – and its customers – continue to benefit from cut-rate financing available from Chinese banks, among other incentives. This activity has picked up as Belt and Road Initiative (BRI)-related projects have got underway. Egypt’s new capital is an example – Huawei is supplying nearly all of the new telecom network infrastructure for an entirely new city intended to house 6.5 million.

Given Huawei’s position as a powerhouse in the developing world, it’s impossible to discuss 5G without addressing Huawei’s prospects.

5G not a rush in low ARPU markets

In developing regions such as CIS, Latin America (LA), and Sub-Saharan Africa, 3G remains the primary mobile connection technology. While 4G will overtake 3G soon even in these low ARPU markets, 5G will take years to emerge. According to stats from the GSMA, these regions will respectively see 5G account for 12%, 8%, and 3% of their total connections by 2025.

These are cellular connections and don’t factor in IoT – a big caveat given 5G’s promise for device to device connections. However, the point remains that 5G will be a slow evolution – telcos like to stretch the life of technologies whenever possible.

That’s especially true for telcos with high debt levels – and there are a lot of these. The net debt (debt minus cash) of the global telco sector was roughly half of revenues in 2018, having been in the 30-40% range of revenues at the cusp of the LTE buildout cycle. Few telcos have room in their budgets for a 5G capex splurge. Even if there are 5G trials underway across the developed world, the developing world will need 10 years or more for widespread migrations to complete.

Individual operators reflect this different pace. Etisalat for example is already advertising ZTE-provided 5G in its home market of the UAE ($41K GDP per capita); however, in the west African country of Togo ($617 GDP per capita), its local unit Moov Togo only launched 4G in mid-2018. There is little need or incentive for Etisalat to push 5G anytime soon in Togo.

The natural conservatism of telcos is heightened when lots of things are changing on the supply side. Right now, Huawei-related uncertainty is slowing down procurement. Even if a product is on the shelf, a telco needs to know it can be supported after the sale. Given that some countries are considering restrictions on Huawei, it’s only natural for telcos to take a breath.

Supply side push likely from Huawei

Any good vendor sales rep talks to customers frequently about new products, in search of interest and/or commitments. Huawei has been especially proactive about stirring up business in small markets like Togo, and successful in turning single-country projects into much larger ones. If Huawei can keep its supply chains running – although this is not certain – it will likely launch an aggressive supply side push for 5G in its strongest developing markets (e.g. Thailand). We can expect more low-cost financing, joint R&D facilities, university partnerships, tie-ins with Huawei’s device and cloud business, and lobbying. Huawei wants to seize the moment.

This could all end up being good for operators if they play it smartly. A better pitch from Huawei should provoke its rivals into doing the same, ultimately benefiting telco customers. The complication is on the financing end and the use of China’s state-owned banks – primarily CDB and Ex-Im. Politics are by definition part of the decision-making process of these banks, and telcos may not want to embroil themselves in that process.

This is now a political issue, as concerns about foreign debt levels grow. Just last month the Kiel Institute for the World Economy issued a report on “China’s Overseas Lending”, noting that for the 50 main recipients of Chinese direct lending, “the average stock of debt owed to China has increased from less than 1% of GDP in 2005 to more than 15% of debtor country GDP in 2017.” The study also found that “about one half of China’s overseas loans to the developing world are ‘hidden’”.

Telcos forced to do more with less as webscale operators splurge

Telcos’ network department headcounts and R&D budgets have been declining for many years. This has made telcos more reliant on vendors for knowledge and technical support, and even rudimentary design. In effect telcos have outsourced much of their R&D to their suppliers. This tends to benefit incumbent vendors.