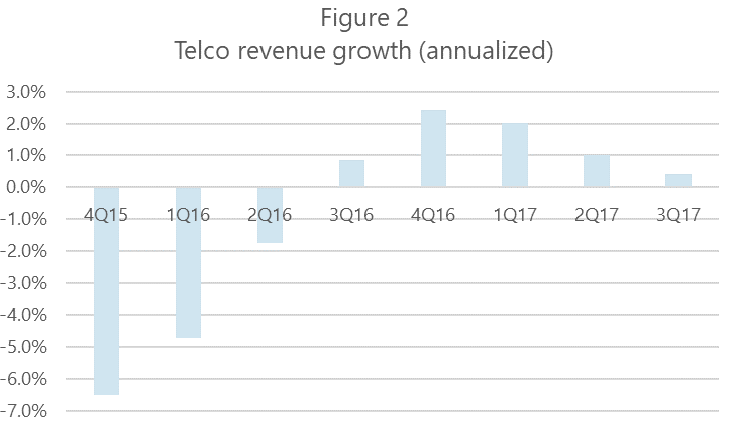

In the six years since India’s last telecom sector reform, operators have made big investments in their networks, the country’s subscriber levels have grown, and prices have declined. 4G is now well established, and fixed line broadband finally has decent prospects .

Local (aka indigenous) vendors have sat on the sidelines, unable to keep up

While telecom has grown in India, local suppliers have not. India has many globally competitive companies in the IT services and software space, such as TCS, Wipro and Infosys. But hardware manufacturing remains a challenge. The bulk of telecom capex goes to foreign vendors, who dominate Indian markets for wireless base stations, transmission equipment, and data/IP gear. Most local equipment vendors, such as ITI, HFCL, and even Tejas Networks, rely heavily on government set-asides.

This imbalance is reflected in trade data. Over the 5-year 2013-2017 period, imports of telecom equipment were an astounding $58B more than exports in India. Imports have been 10x the value of exports, or higher, in the last three years. (Figure 1).

For the 2012-14 timeframe, 4G network equipment accounted for a good chunk of the deficit. Since then, the smartphone boom has driven deficits higher. Indian regulators started addressing this in 2017, by imposing a 10% duty on smartphone imports. That has been increased twice, and is now at 20%.

The import duties have encouraged foreign device companies to increase local production. That includes an announcement last week from Xiaomi: its supply partner Holitech Technology will build a factory in Tirupati, employing up to 6,000, and producing camera modules, transistors, touch screens, flexible PCBs, and sensors. This adds to Xiaomi’s already significant local production in India. Samsung, Huawei and others also have facilities.

However, even with some handset production now done in India, much of the value added still comes from overseas. Per Ministry of Commerce trade data, parts account for 30-40% or more of total telecom equipment imports (in value). High-end components for handsets are one part of this. The same issue arises with production of network equipment (e.g. routers): even when produced locally, many of the component parts are imported. That includes semiconductor content in particular.

Further, when foreign vendors set up factories in India, it’s generally to sell gear into local markets, not for exports. There are notable exceptions to that, some in the network infrastructure space: for instance, Ericsson’s Pune plant exports microwave gear to Africa, Southeast Asia and other markets. But the value of these exceptions are small, relative to the huge volume of locally produced & sold gear.

Regulators try again: TRAI’s latest report

As India’s telecom deficit has grown, the government has not ignored the problem.

In Sept. 2017, the Telecom Regulatory Authority of India (TRAI) issued a consultation paper, on the topic of promoting local manufacturing of equipment. The paper addressed the trade deficit issue, and highlighted as the primary cause “relentless” competition from China, “known for large-scale production and export of low-cost equipment”. Imports from Sweden, Finland and America were secondary factors.

Earlier this month, the TRAI concluded its inquiry on the topic. The final report is a comprehensive assessment of the factors limiting India’s ability to compete in telecom equipment markets. The document is impressive as an analytic effort. It identifies a wide range of factors & prescribes recommendations in each area: from university training to patent protection to customs reform to the creation of a number of new boards and agencies.

However, it lacks focus. It suggests doing a bit of everything, and with little new funding: for example, the TRAI’s recommended “Telecom Research and Development Fund” (TRDF) would be equipped with $170M at the outset. That’s better than the status quo, but hardware startups are expensive. One of the smaller US venture capital funds focused mainly on communications technology, Kodiak Ventures, manages $681M or roughly 4x that of the proposed TRDF. The most promising India-based startups are not likely to work with a government VC fund that cannot offer competitive levels of funding and other support.

5G is an opportunity, in theory

In the near term, one intriguing opportunity for vendors – whether local or not – is in fixed broadband, where FTTx rollouts are underway at several companies, including Jio, Bharti Airtel, and BSNL. In the longer term, the shift to 5G is a far bigger opportunity.

While India was late to 4G, policymakers hope to change that with 5G. As India’s Telecom Minister, Manoj Sinha, stated recently, “We missed [the] 2G, 3G, and 4G bus but we are not going to miss [the] 5G bus. A lot of work has been done in our department” to ensure that.

India’s Telecom Secretary, Aruna Sundararajan, has been outspoken in saying India should embrace 5G aggressively, not just for services but to help develop India’s export sector. She is also plugging C-DOT as a technology developer. At the MWC event in Barcelona this year, she met with a number of global tech vendors, commenting that “all the players are positioning themselves for India as a big 5G market. One of the leading chipset [suppliers] in a meeting told us that India will have one of the biggest IoT user base[s] and the company is keen to partner with C-DOT for developing various IoT solutions.”

Beyond enthusiasm, the government is making some modest direct investments in 5G. For instance, C-DOT announced in Feb 2018 that it would set up testbeds in Delhi and Bangalore, led by Anurag Gupta (who attended MWC for C-DOT). The goal is to set up the testbeds in phases, starting with the first in Dec. 2018. C-DOT also signed agreements in June 2018 with three UK universities to conduct joint 5G R&D in several areas, including massive MIMO and mmWave.

In addition, India’s IITs recently announced a 5G commitment from the Telecom Department. Press reports suggest a budget of ~$75M, supporting the work of around 200 engineers. The IIT 5G project will create testbeds across all 5 IIT campuses. At its Delhi campus, IIT will also work with Ericsson on a new 5G “Center of Excellence,” focusing on massive MIMO R&D.

C-DOT could play an intriguing role

The TRAI report suggests creating several new boards and councils, some multi-agency. To a skeptic, this sounds like a recipe for delay and indecision. That same skeptic might wonder if India already has a well-established organization charged with the development of local telecom equipment production.

The Centre for Development of Telematics (C-DOT) is an autonomous agency of the Indian government focused on R&D in the area of telecommunications. It has just over 1,000 employees across two main R&D campuses, in Delhi and Bangalore. C-DOT develops technologies & licenses them to both government-supported entities such as ITI, and local private sector companies like Tejas Networks.

C-DOT’s employee count has grown in recent years, and it has picked up the pace of its transfer of technology (ToT) announcements. Recent policy changes give C-DOT the charge to seek out overseas business more actively. Under the government’s “Synergy Plan” released in January 2018, C-DOT is to work with ITI and Telecommunications Consultants of India Ltd (TCIL) on future exports of products & services. That includes granting a manufacturing license to ITI for C-DOT’s terabit router.

Several C-DOT partners, including ITI and BEL, are actively looking to increase exports with the help of C-DOT product. C-DOT executives have appeared recently at public conferences, making a direct pitch to help Indian manufacturers increase exports.

R&D wholesale model, limited funding both need to be addressed

While C-DOT has potential to contribute to 5G and other areas, it is currently viewed as merely a government R&D institute, in effect a wholesaler of R&D to local vendors. C-DOT’s manufacturing partners are responsible for implementation and customer support. To thrive, C-DOT will have to participate more fully in individual projects, getting their hands dirty and talking to customers. After all, many vendors – notably Huawei – include R&D engineers in all aspects of the process, through field deployment and maintenance. India’s vendors can’t just rely on an R&D outsourcing body, and one which licenses its products to multiple players. For C-DOT to help Indian industry drum up more overseas business, functional changes will be needed, along with significantly more funding. As a reference point, C-DOT’s entire budget for fiscal year 2016-17 was about $60M. In 2016, Huawei spent $32M on R&D per day.

-end-

Email Matt

Image credit: Shutterstock

which is a physical data transfer service using a 45-foot long container on a truck. That’s for transport to and/or between AWS data centers. Amazon also continues to “Invest” in (or acquire) cloud-related companies, including cyber security company

which is a physical data transfer service using a 45-foot long container on a truck. That’s for transport to and/or between AWS data centers. Amazon also continues to “Invest” in (or acquire) cloud-related companies, including cyber security company

{kind=link}