Webscale sector’s capex push to bring many more data centers online in 2021-23

Capex surge from webscale operators will continue

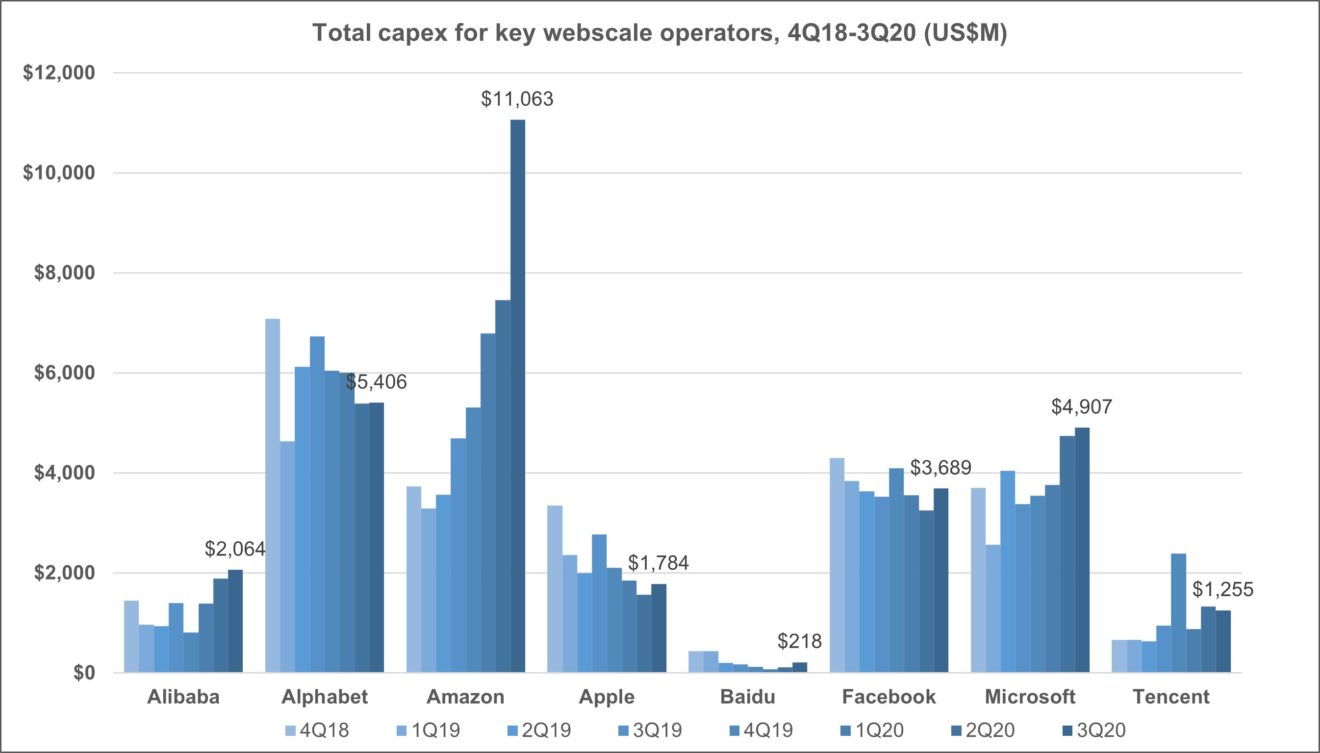

Technology spending by the webscale sector is on a tear. While COVID-19 depressed the telco sector in 2020, strong demand for cloud services and ecommerce drove the webscale operators providing these services to expand investments considerably. Webscale capex rose 25% YoY to hit $34.7 billion in 3Q20, or $120.9 billion on an annualized (12 month) basis. That amounts to 42% of the telco industry total for the same period. Just three years prior, in the 3Q17 annualized period, webscale capex was only 24% of the telco market.

The webscale market is dominated by a small number of big spenders. Alphabet, Amazon, Facebook and Microsoft captured 70% of sector capex in the last 4 quarters, Apple added 6%, and each of China’s two big players (Alibaba and Tencent) added another 5% each. Going forward, China will account for a bigger share of the total, possibly as much as 20% by 2025.

As a reference point, the figure below illustrates recent single quarter capex trends for the 5 biggest US-based and 3 biggest China-based webscale providers.

Source: MTN Consulting

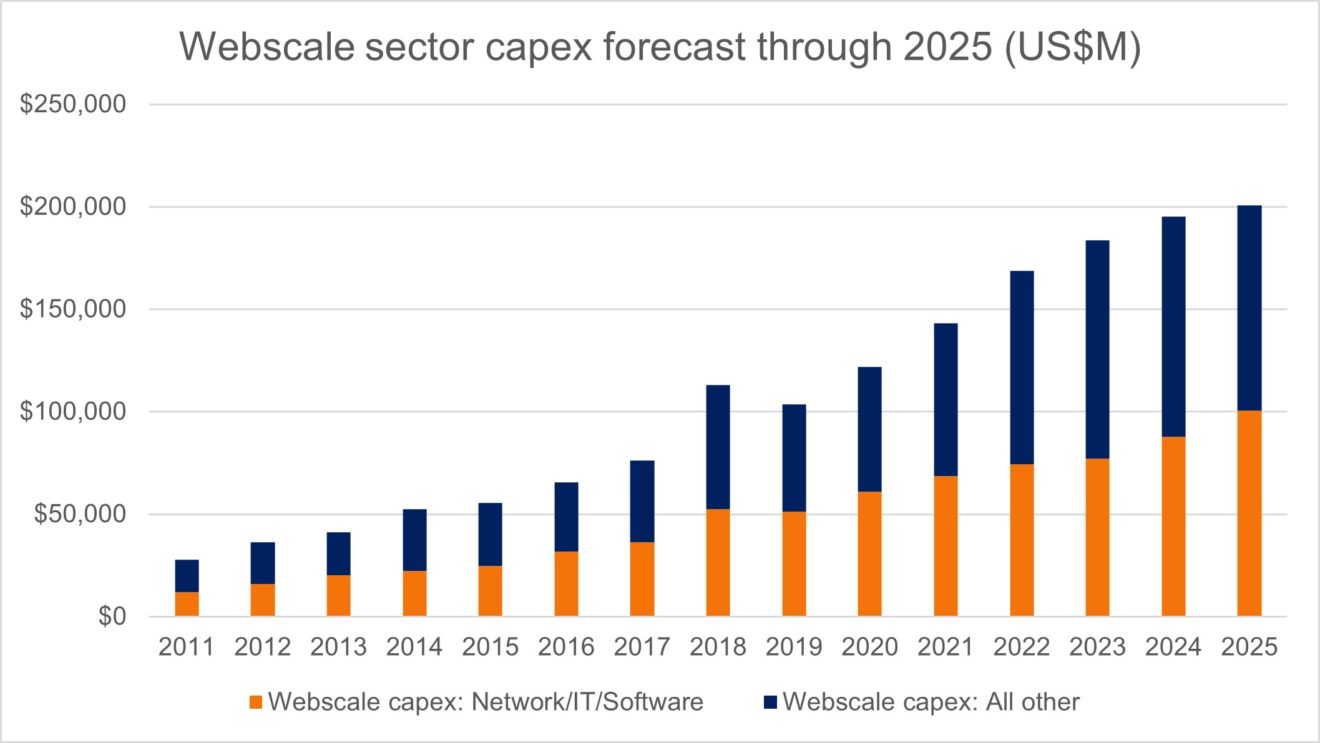

The growth in 3Q20 wasn’t a one-time thing. While the outlook for telco capex is modest, MTN Consulting expects webscale sector capex to end 2021 at roughly $143 billion, and grow further to reach approximately $201 billion by 2025 (figure, below). The network/IT/software portion of capex will come in at roughly 50% of total in 2020, as it did in 2019, decline to 42% by 2023 as a spate of new data centers come on line, but grow back up to 50% by 2025 as more of capex is for server/capacity expansion of existing infrastructure. Within the technology piece of capex, data centers and their components (networking, compute, storage, power) will soak up the bulk of spending, but subsea cables and satellite networks will become increasingly important over the next 5 years.

Source: MTN Consulting

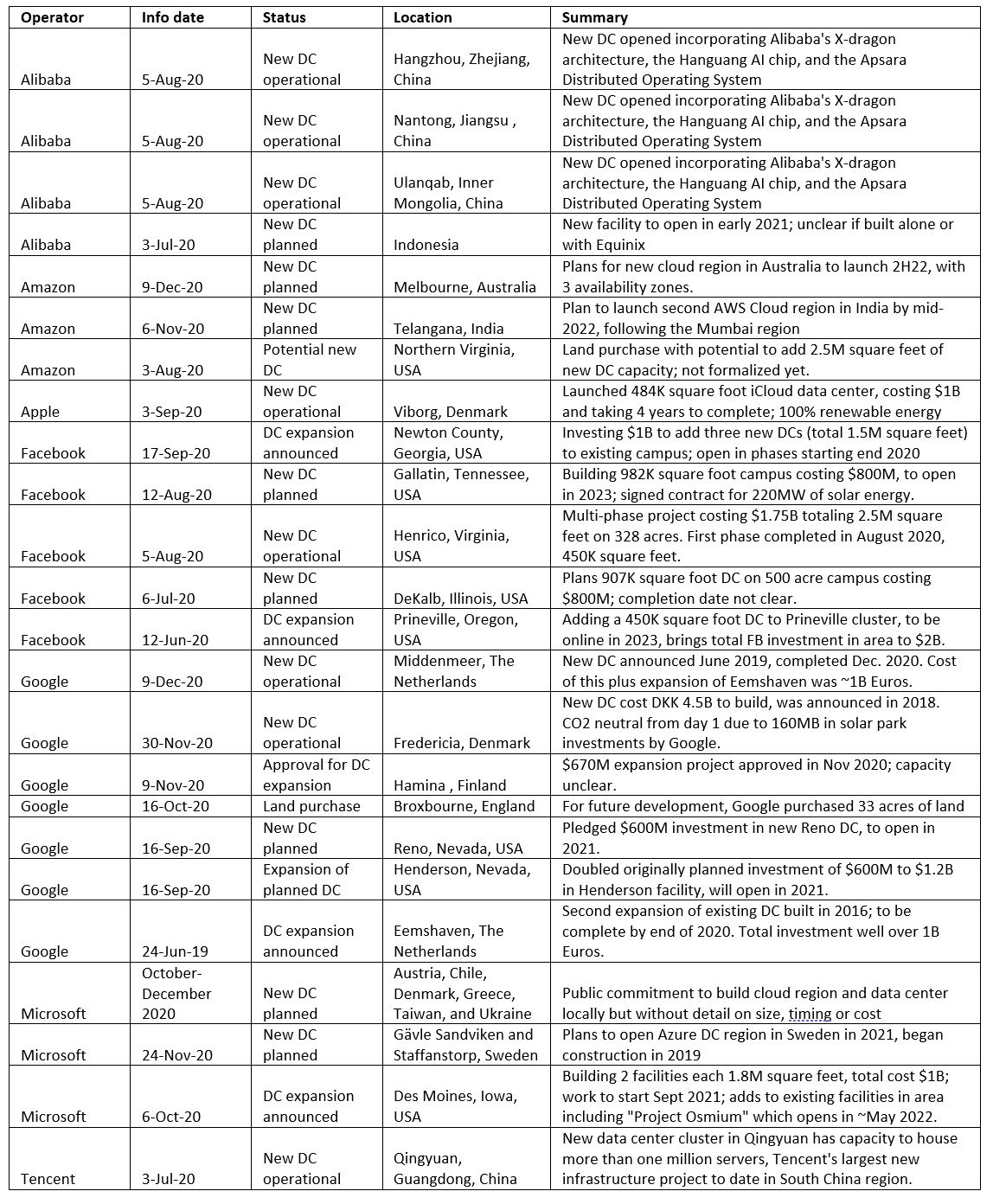

All of the big webscale providers have major data center construction or expansion projects underway, in multiple corners of the world. Some of this activity leans on partners from the carrier-neutral sector, for instance Oracle is relying heavy on leased collocation space from Equinix for the Oracle cloud buildout. However, the bulk of webscale capex is aimed at enormous, self-owned facilities designed to spec. The choice of location is crucial, and depends on many factors, including access to major population centers, big customers, submarine cables, internet exchanges, and low-cost renewable energy; government incentives such as tax abatements; and how the location complements the operator’s overall global network strategy. Because location is so important, many webscale providers buy land in attractive markets far in advance of a decision to build a data center; this is known as “land banking.”

Below is a brief summary of some of the webscale sector’s major data center projects, either currently underway or recently completed.

Table 1: Data center projects underway – a snapshot

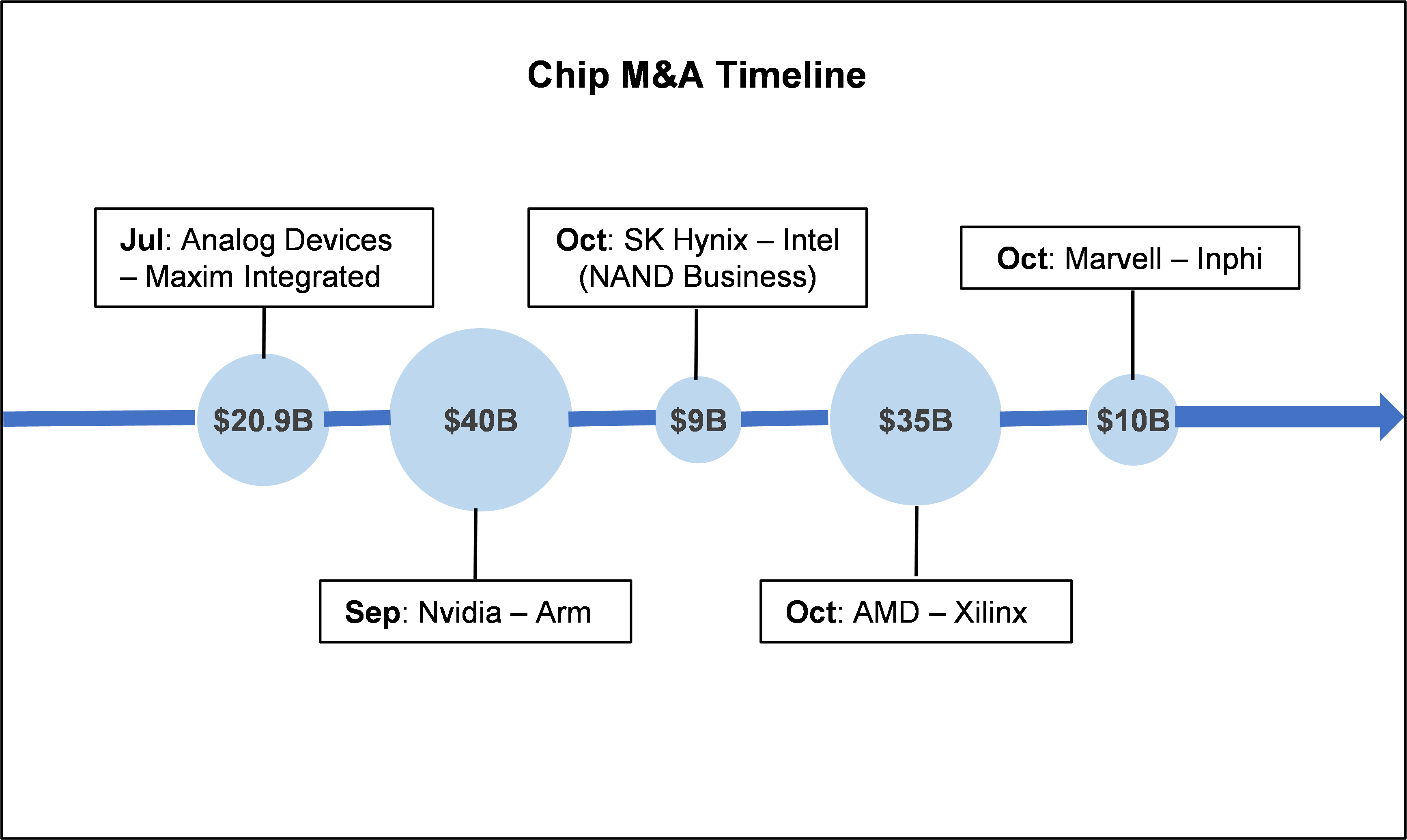

After a prolonged hiatus, M&A activity in the semiconductor landscape ramped up significantly this year, nearing the record levels of 2015. The consolidation surge was particularly notable during the second half of 2020. These deals targeted many end use markets but the common thread is the cloud data center market: remote work and study amid the COVID-19 pandemic has spiked demand for cloud-based tools and services. The dealmaking is not yet done. Next year is likely to witness more consolidation among chipmakers, despite geopolitical tensions between the US and China and stringent regulatory scrutiny serving as impediments to deal completion.

Flurry of chip deals bring cheers to an otherwise muted first half

Chip M&A activity had a quiet first half of the year, as COVID-19 created high levels of uncertainty and steep drops in GDP. Stock markets settled in 2H20, though, and big companies found ways to operate amidst a pandemic. COVID-19 remains a severe problem for many major economies, but improved business sentiment and a gradual economic recovery have fostered a strong climate for M&A.

With year-to-date announced deals already topping $100B in value, 2020 is turning out to be a blockbuster year for chip M&A. The mega-deal kickstart to the chip M&A frenzy was Analog Devices’ $20.9B acquisition of rival chipmaker Maxim Integrated Products in July 2020. This was followed by Nvidia’s acquisition of chip design house Arm for $40B in September 2020, the year’s biggest deal so far. The month of October saw a string of M&A agreements featuring the $9B acquisition of Intel’s NAND SSD business by SK Hynix, AMD’s $35B deal to acquire Xilinx, and Marvell’s $10B acquisition of Inphi.

Figure 1: Timeline of semiconductor M&A in 2H20

Source: MTN Consulting

Chipmakers aim at the lucrative cloud data center market

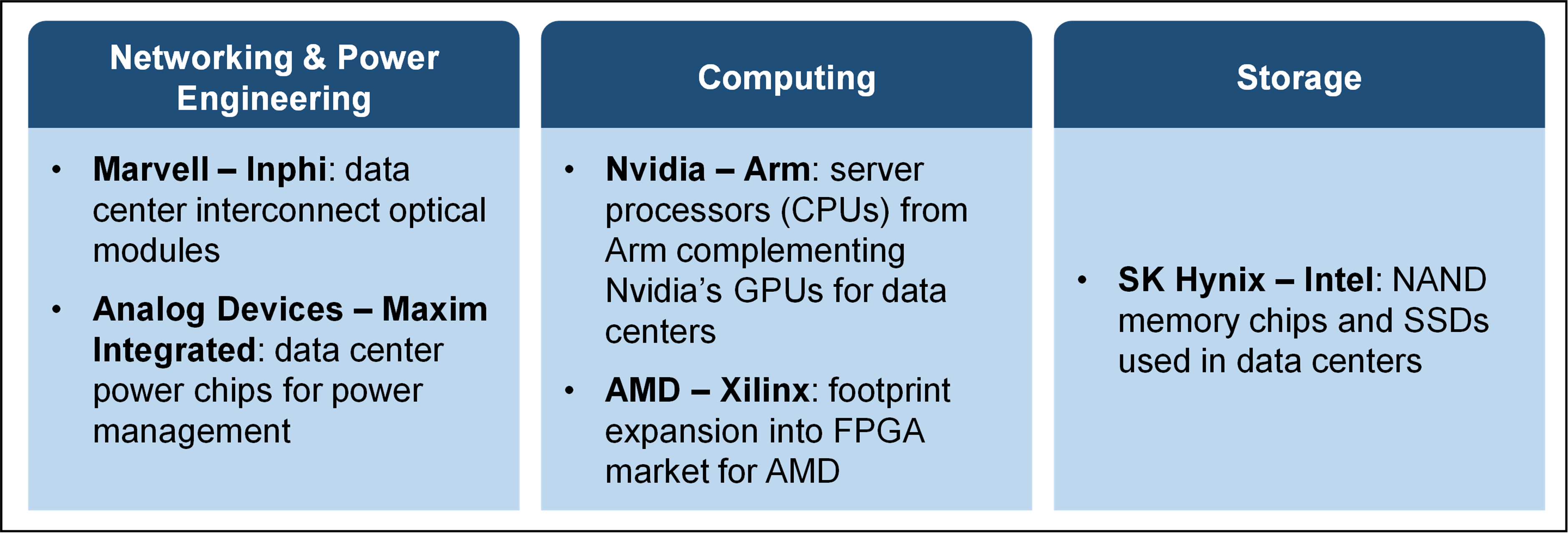

None of the big chip deals are focused narrowly on a single end market, but one key market is of common interest to all – the cloud data center. The deals differ from each other in terms of sub-market focus, though, stretching from power engineering and networking, to computing and storage – see Figure 2 below:

Figure 2: Data center aspects of 2020’s big chip M&A transactions

Source: MTN Consulting

Networking & Power Engineering

Networking and power management form the vital foundation of any data center infrastructure. Optical modules help connect not just the server racks inside data centers but also the data centers to one another across different locations. With the acquisition of Inphi, Marvell aims to target this space by providing interconnect solutions that enable seamless and speedy movement of data between and inside data centers.

Chips for power management have grown in significance over the years to control the biggest expense of running a data center, i.e. power utility costs. Analog Devices is seeking to address this issue through Maxim Integrated’s data center power chips, which also permit greater computational capability to data center operators.

Computing

Data centers typically house thousands of servers that process and run applications along with high performance computing (HPC) workloads. The processing and computational tasks are carried out by server processor chips that come in various forms: CPU, GPU, FPGA (field-programmable gate array), and ASIC (application-specific integrated circuit). Intel, AMD, Nvidia, Xilinx, and Infineon are some of the leading server processor vendors developing either one or most of the chip types.

The acquisitions announced by AMD and Nvidia relate to expansion into new server chip types, and also rivaling Intel as a more formidable force. AMD is looking to dent Intel’s customer base with the acquisition of Xilinx. The FPGA pioneer Xilinx had earlier managed to end Intel’s exclusivity with some its customers such as Microsoft. Meanwhile, GPU maker Nvidia will gain access to server CPU designs through its Arm acquisition. Arm-based server processors are already being adopted by webscalers like Amazon for its data centers. For now, Intel is looking to counter these developments through in-house efforts aimed at the server GPU market for data centers, extending its presence across all the four chip types.

Storage

On the storage side of things for data centers, Intel has agreed to sell off its NAND SSD business to SK Hynix. The assets sold include Intel’s NAND component and wafer business along with the NAND manufacturing plant in Dalian, China, but exclude Intel’s “Optane” memory business. Intel’s NAND memory chips are mostly used in smartphones but also data centers to support in-memory processing demands of the cloud. The business acquisition will elevate SK Hynix’s market share in the NAND memory market, which is currently dominated by Samsung Electronics.

Three key factors are fueling M&A among chipmakers

Three key factors discussed below are driving chip companies to go on a shopping spree:

New applications: Key emerging applications based on AI/ML along with new evolving markets in edge computing, self-driving vehicles, and 5G have opened new frontiers for chipmakers. This is in addition to the ever-increasing demand for more media-intensive content such as images, audio, and video streaming over cloud that require faster server processors and networking capabilities for seamless and speedy transmission to end users.

Faster time to market: Apart from the obvious reasons of expanding into new markets and accessing proprietary technologies, chipmakers are increasingly exploring M&A to cut down on the costly and lengthy R&D timeline associated with developing advanced process nodes and chips, thus enabling faster scaling. Slowdown in Moore’s law is also pushing chipmakers to look elsewhere.

Improved market conditions: A low interest rate environment has enabled chipmakers to borrow modestly and finance acquisitions. Rising stock prices are also aiding large chipmakers such as AMD and Nvidia to fund their purchase either partially or entirely in stocks. Notably, Nvidia surpassed Intel as the largest US chipmaker by market cap in July 2020

More chip industry consolidation on cards but not without hurdles

The M&A activity in the chip market landscape is likely to continue into next year, but probably not at the scale of what has transpired so far in 2020. Even though the deal-making drivers discussed above will persist in 2021, future deals may confront more obstacles related to COVID-19 and geopolitics.

With COVID-19 expected to play out well into 2021, delays in deal-making would keep the deal volumes limited as carrying out negotiations, due-diligence, and audits would be challenging with travel restrictions and limited in-person meetings. For companies having long-term or strong working relationships with prospective acquirer or targets, the pandemic would be less of a worry, as seen with Nvidia-Arm or AMD-Xilinx for instance. These pairings shared strong working relationships prior to acquisition.

Geopolitical tensions between the US and China upsets the stability needed to make M&A deals happen. That’s especially true in the chip sector. With the situation not expected to get any better even under the Biden administration, China has been gearing towards chip self-sufficiency by pouring billions of dollars to support the growth of its domestic chip industry and advanced chip development. Furthermore, open-source chip architectures such as RISC-V have opened the gates for Chinese tech firms like Huawei. Chipmakers will be wary of snapping up companies amid a hostile business climate.

Last but not the least is the regulatory hurdle that an M&A transaction must go through before the final deal closure. Big-ticket deals are subjected to increased scrutiny due to wide-ranging issues such as strict antitrust laws, national security threats, access to proprietary technology, and sanctions imposed under trade disputes. All the chip M&A deals discussed above are pending regulatory approval, in multiple jurisdictions. Among them, the Nvidia-Arm deal is likely to raise eyebrows among the watchdogs, especially in Europe and China. China could essentially prove to be a spoilsport in the Nvidia-Arm deal: Chinese tech firms currently use UK-based Arm’s intellectual property to design chips, which could change post acquisition by US-based Nvidia. If China blocks this transaction, it would not be the first time. Two years ago, China blocked US-based Qualcomm from completing its acquisition of the Netherlands-based chipmaker NXP Semiconductors.

“The COVID-19 impact is, of course, hard to assess…”

With this comment, Ericsson’s CEO has captured the general sentiment of the market. Many tech companies to report earnings over the last 1-2 weeks have withdrawn financial guidance. That includes Avnet,Infosys, Sanmina, and Wipro. Some have provided guidance for the next quarter only, but withdrawn full-year guidance (Harmonic). Chipmaker NXP has provided a high-low range on its revenue forecast, projecting between 14-23% lower revenues in 2Q20 than the prior year period. All companies emphasize how unstable the current environment has become, where – as F5 CEO puts it – “COVID-19 has altered just about everything about our daily lives.”

New economic forecasts emphasize uncertainty, downside risk

As we covered in our last newsletter, the IMF issued its latest World Economic Outlook on April 14. That called for a three percent contraction in global GDP in 2020. While the COVID-19 curve may be flattening in some countries, the economic outlook remains stark. An advisor to US President Trump says US GDP could drop as much as 20-30% in 2Q20. JP Morgan expects the second quarter drop to be even worse, projecting a 40% decline. Europe also faces a recession; for full-year 2020, the Bank of America expects GDP to fall nearly 8%. Oxford Economics expects world trade in goods and services to fall by 10-15% in 2020.

The prospects for the China market are, in theory, better than countries more recently dealing with COVID-19’s spread. China is getting back to work in 2Q, after all. However, reliable information from China on COVID topics continues to be limited. Like other countries, China could face a double dip if things are loosened too quickly and a second lockdown is required. There are political risks to the current regime given both pressure from the US and domestic frustration. Moreover, nearly every tech manufacturer is now re-evaluating their supply chain strategy, looking to enhance resilience and lower China’s leverage.

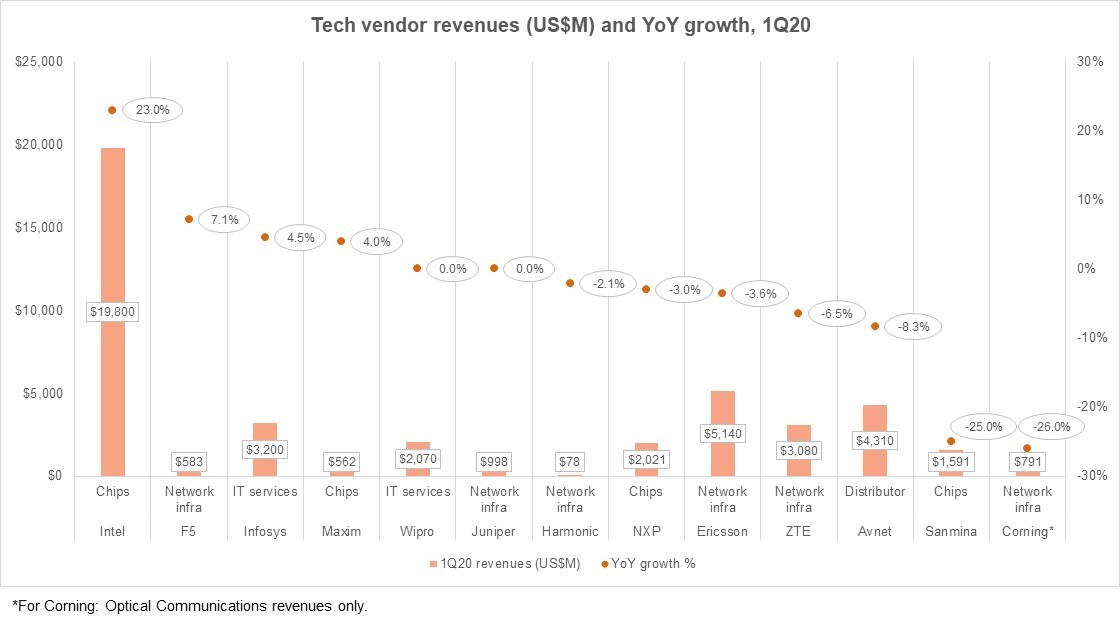

Vendor revenues started showing signs of weakness in 1Q20

The biggest tech vendor to report 1Q20 earnings so far may be chip specialist Intel, which reported a surprising 23% growth in revenues to hit $19.8B. Intel found itself in a sweet spot of growth with its Data Center Group in 1Q20, whose revenues rose 43% to $7B. Even the telco (comms service provider) segment of DCG saw double digit growth, up 33% YoY. Intel is an exception though, and it expects its own growth to moderate to 12% in 2Q20.

Other chip companies didn’t do quite so well. Maxim reported 4% YoY revenue growth in 1Q20, while NXP and Sanmina saw revenue declines of -3% and -25% respectively. Revenue decline was worse for NXP and Sanmina in their communications segments, down 10% (NXP Comm Infra) and 38% YoY (Sanmina Comms Networks).

A number of the biggest vendors active in the telecom network infrastructure segment

have reported, including Ericsson, ZTE, Juniper, F5, and Harmonic. F5 reported a 7% growth in revenues, to $583M, and Juniper reported flat revenues at $998M. All others reported YoY revenue declines (on a US$-basis) in 1Q20. Ericsson corporate revenues fell 4% YoY, while networks revenues dropped at a more modest 0.6% YoY rate due to an uptick in new 5G network deployments. Corning revenues fell 15% overall in 1Q20 to $2.39B, but optical communications revenues to telcos/CSPs dropped faster, down 27% YoY to $568M.

Two large IT services vendors, Wipro and Infosys, have done slightly better than some of their hardware-focused counterparts. Infosys corporate revenues increased 4.5% YoY to $3.2B, while Wipro stayed flat at $2.7B. Communications sector revenues were flat for both: $416M for Infosys (from $413M in 1Q19), $114M for Wipro ($118M).

One other early reporter is Avnet, an electronics parts distributor with a peripheral role in the network infrastructure supply chain. Avnet’s revenues dropped 8.3% YoY in 1Q20 to $4.31B. This is one of the companies which withdrew guidance for 2020. Avnet’s commentary by region is interesting, and optimistic in places. It is “cautious” about the Americas and expects a drop-off in revenues in EMEA, but the rest of Asia is mixed, and “Greater China is operational and appears to be recovering.”

The figure below illustrates reported 1Q20 revenues for the companies mentioned, along with the YoY growth rate.

Implications of earnings

A few trends are apparent from a review of early earnings reports.

Companies are spending a lot of time rearranging operations to support working from home (WFH). Employee safety is the key priority for most companies right at the outset. This is not a small task, as some of these vendors are huge and accustomed to team working environments. Ericsson says that about 85,000 of its employees now work from home; for Wipro, it’s 90% of 165,000 employees. Transitioning to WFH while getting work done and keeping customer satisfaction high is the ultimate goal. On that note, Wipro says its SLA performance on services contracts was stable in 1Q20. More companies may need to address this directly.

Networks may be largely software-based nowadays but building and maintaining them still requires human interaction. As such, vendors have had to modify processes to ensure customer safety, too. This hits telcos harder, especially fixed network operators who need to install or maintain service in residential units. That’s something to watch as telcos report.

Cloud and data center spending in general appeared to hold up better in 1Q20 than telecom, and lifted several vendors. Some of this is due to COVID’s (modest) positive affect on cloud usage in general, and services/apps that cater to the work (and study) from home market. Webscale operators continue to make big investment announcements. Facebook pushing into India with its Jio tie-up is one. Equinix announced a $1B joint venture with GIC to build data centers in Japan. There is even a rumor that Rackspace is hoping to go public (again) in 2020. Public equity markets will need to stabilize before the IPO market kicks up, though.

Vendors are spending more time and ink addressing their liquidity position than usual. Faced with a potentially double digit drop in global GDP in 2020, they have to consider the long-run. Some companies won’t make it. And when you choose your supplier, their financial viability in this climate needs to be a primary criteria.

Changes in tech supply chains are underway. Companies need to diversify sources away from China, most important. The trade war started this, and COVID-19 will give it new life. For IT services vendors, this is an opportunity for them to advise other companies, and help to foster new processes and value chains. TCS notes that it is “helping customers re-orient supply chains to ensure resilience and meet critical needs.” For most vendors, it is about better managing risk. Ericsson notes that its strategy “since long has been to secure a dual mode production,” regularly conducting continuity assessments including multi-source component sourcing. Smaller vendors will have to address the issue too, and it will stress some. The need for more resilient supply chains will add to the industry’s momentum towards consolidation.

As the four-way tussle unfolds among the top tech giants – Apple, Amazon, Google, and Microsoft – for the “world’s most valuable company” tag, Apple could be covertly prepping its entry into the fast-growing cloud computing space.

Ironically, a big operational chunk of Apple’s services (Siri, iTunes, Apple Music, etc.), rely on third-party cloud providers. For instance, Apple apparently shells out US$30 million per month for Amazon’s cloud services and also employs Google’s cloud services. It has also reportedly used Microsoft’s Azure platform.

Despite spending massively on renting cloud resources, the iPhone-maker has been plagued by network outage troubles, along with privacy breach concerns in the past. These issues have compelled Apple to beef up its own data center infrastructure to wean itself from reliance on rival cloud providers. Up until now, Apple‘s cloud presence is limited to iCloud, which is essentially a SaaS-based content storage offering for consumer markets – much different from what big cloud rivals offer.

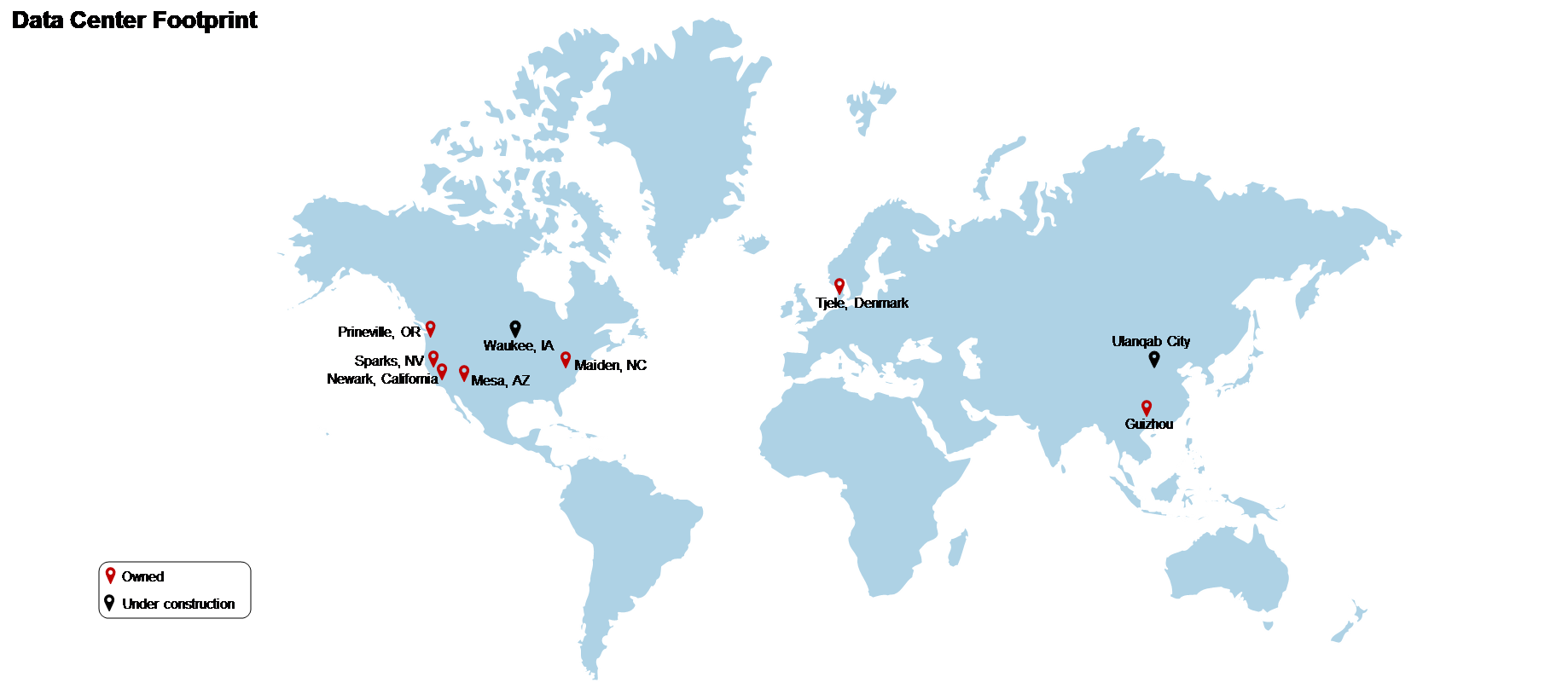

Due to recent expansion efforts, Apple currently owns a total of nine data center sites worldwide, out of which two are under construction (see footprint map below). These data centers meet Apple device users’ demand for services such as iTunes, iCloud, and Apple Music.

Source: MTN Consulting

These nine data centers are also a nice starting point for a cloud business. Apple needs far more infrastructure of its own, but we believe that Apple will look to target the enterprise market with its own cloud computing solutions. Below are a few rationales to suggest that Apple is on its way to make this long-term goal a reality.

#1. Exploring revenue diversity to cut business dependence on iPhone sales

Apple’s flagship product and cash cow, iPhone, continues to drag the overall top line. Annualized sales revenues from iPhone declined by 14% YoY in 3Q19. As a result, total company annualized revenues declined by 2% YoY during the same period.

The iPhone accounts for more than half (54.7%) of Apple’s total annualized revenues in 3Q19. However, it battles declining loyalty among customers who feel less motivated to buy/upgrade due to less-valued features. Customers are being obliged to pay Apple’s premium mostly for improved camera capabilities in newer models as they are still functionally identical to the iPhone X launched in 2017. To offset its impact partly, Apple is now focusing on non-flagship businesses in “Services” and “Wearable, Home and Accessories”.

The Services business, Apple’s second biggest segment, along with the Wearables unit will be key in the near term as sales of iPhone are likely to remain sluggish. The Services unit doubled its contribution to Apple’s total topline since 2015 from 9% to 18% in 2019, implying the growing clout of the segment.

But there is a downside – Services and Wearable units are mostly dependent on iPhone sales because they largely operate on handset devices. This is where Apple’s own cloud offerings turn into a desirable plan as it would remain relatively immune to such business inter-dependencies.

#2. Existingefforts to revamp infrastructure (Pie and McQueen) support a cloud push

Apple’s cloud quest commenced around 2016 with an infrastructure restructuring program for merging its services (including Siri, iTunes, Apple Music and Apple News) onto a single proprietary cloud platform called “Pie”.

Apple is physically relocating its employees in cloud services and related departments scattered across various locations at one place under this project. The aim is to have more control on the infrastructure and resources for improved user experience.

Apple also kicked off a self-sufficient cloud infrastructure project called “McQueen” a few years back, in a bid to reduce dependence on other leading cloud vendors such as Amazon and Google.

In line with this, Apple announced investments of US$10B late last year to build new and expand existing data centers across the US over a five-year period. Out of this, ~US$4.5B has been likely spent so far.

Apple is also expected to open its first data center on the Chinese mainland (Guizhou province) by 2020, construction of which has picked up speed this year. A second data center in the country is also coming up in Ulanqab City. Both these data centers will primarily host iCloud data of Chinese users.

Currently, most of iCloud’s data is hosted on Amazon’s AWS or Google’s GCP, according to the iOS Security Guide published by Apple. The current expansion drive will reduce Apple’s reliance on third-party cloud vendors.

Once the objectives of both these projects are achieved, Apple could look to venture into the public cloud market – exactly how Amazon started out, i.e. by meeting its own cloud needs first and then renting out excess cloud capacity to the enterprises.

#3. Rising cloud demand driving rivals’ business growth

Amazon, considered to be the cloud pioneer, continues to achieve glory and robust business growth in the cloud market through new business models despite being in existence for over a decade. Its cloud computing unit (AWS), which started off as a storage service for its core e-commerce business, has emerged as the most lucrative business and a profit machine – AWS has consistently accounted for >50% of Amazon’s overall operating income per quarter this year.

Microsoft is slowly catching up with Amazon in the cloud race, as its cloud business is growing from strength to strength and driving the company’s overall business. In 2Q19, Microsoft’s cloud segment, which includes Azure cloud, emerged as the biggest business unit.

Google’s cloud offering might be a distant third behind AWS and Azure but is making modest advances with aggressive pricing strategy in the cloud arena. The Google Cloud segment, which includes its public cloud offering Google Cloud Platform (GCP) along with G Suite tools (Gmail, Hangouts, Calendar, Google+ and Docs), now generates US$8B in annual revenues.

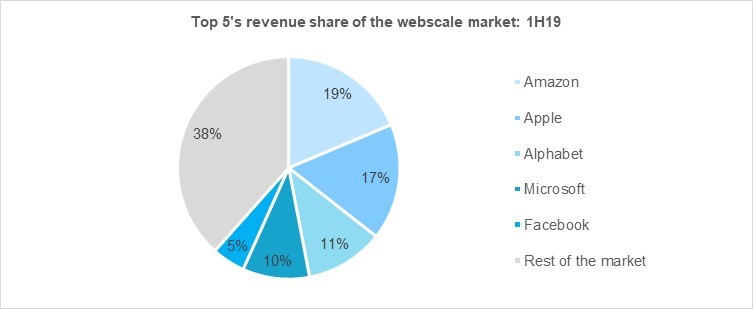

With strong earnings and growth still being reported by the “Big Three” cloud providers, Apple could be motivated to replicate the success of its rivals. Out of the top 5 webscale network operators (WNOs), only Apple and Facebook lack cloud offerings (see chart below).

#4. Strong M&A appetite to enter new focus areas

Apple’s recent billion-dollar acquisition deal involving Intel’s smartphone modem business reveals the company’s strong desire for M&A to pursue new priorities. The deal ensured Apple’s entry into the 5G-enabled handsets race, albeit a bit late.

With a strong kitty of cash and short-term investments worth US$100.5B at the end of September 2019, Apple could go for a similar deal within the cloud space. But instead of acquiring a cloud player, the iPhone-maker may have other plans.

Since Apple already has expertise in building cloud infrastructure somewhat with its own data centers, it could instead look to buy a chip company (or assets) that would develop customized chips to power its data centers – a ploy already in practice by cloud rivals. Interestingly, Apple is building in-house custom ARM-based chips for its future Mac lineup.

Like 5G, Apple’s potential entry in the public cloud market would again be relatively a late one. To counter established cloud rivals, it would have to compete on network security and reliability, making a chip company acquisition more sensible for Apple.

Potential target market could be much beyond developers

Apple’s initial aim would be to catch the low-hanging fruit – the iOS developers’ market – to sell its cloud offerings. Apple is known to create solutions and platforms that are purposely built for its own ecosystem, and its potential cloud offerings would not be any different. This is one of the aspects developers would lean towards, especially for the development of iOS-based applications, as they could access interfaces and platforms in tune with Apple’s ecosystem for OS development.

Privacy and security are Apple’s priorities with its current portfolio of devices and services. These attributes would help Apple target high-value cloud clients. Government cloud deals, which are always sensitive, are a potential target for Apple. The recent US$10B cloud deal between Microsoft and the Department of Defense is an example.

For small-and-medium enterprises and users with limited IT expertise, current offerings from Amazon and other cloud providers are complex to use. This is where Apple could tap the “bottom of pyramid” with an intuitive and easy-to-use cloud platform.

Despite expansive efforts, Apple may still fall short of becoming a formidable cloud force

The cloud trio of Amazon, Microsoft, and Google would undoubtedly be impacted by Apple’s potential entry to the cloud scene – they would lose a customer (or potential one) and gain a competitor. But Apple is known to focus on high-end markets with priority to profits over market share. Apple may not offer mass-market cloud solutions as its rivals do – just as its iPhones are targeted at a premium consumer base. Apple’s purpose would be to offer reliable cloud computing solutions that operate in its own ecosystem and provide a quality user experience. All this could also end up being a futile endeavor for Apple due to its inexperience relative to cloud rivals. High profile acquisitions or hires will help, though, and Apple has plenty of cash for both. Apple taking the “cloud” path could prove to be a game-changer in the fortunes of the company that is desperately seeking for a life beyond iPhone.

After taking the Indian telecom scene by storm to reach the pinnacle (by subscriber base) in just three years of commercialization, Reliance Jio Infocomm (Jio) is all set to spread its wings into the booming Indian cloud market. In a 10-year deal with the cloud heavyweight Microsoft, Jio will build new cloud data centers across India that will support Microsoft’s Azure cloud platform to offer economical India-native cloud-based solutions for enterprises. As a part of this, two initial data centers are being built by Jio in the Indian states of Gujarat and Maharashtra – both slated to go live by the end of 2020. These two facilities are reportedly ~7.5MW in capacity, small relative to the largest global facilities but significant for India.

Microsoft has been part of the Indian cloud scene since 2015, before its closest webscale network operator (WNO) rivals Amazon (2016), Google (2017) and Alibaba (2018). Though Microsoft claims to operate three data centers in India, interestingly, these are hosted in a part of existing data center companies such as CtrlS Datacenters and Netmagic (so do Amazon and Google). The partnership with Jio also has a similar set up – Microsoft’s Azure Cloud hosted on Jio’s data centers. By contrast, Microsoft’s recent cloud partnership with AT&T will likely have the telco relying primarily on Microsoft built infrastructure.

The Jio-Microsoft deal also marks telcos’ greater engagement in the Indian webscale arena offering cloud and network connectivity solutions, with Airtel already in the backdrop for quite some time – Airtel operates a wholly-owned data center unit, Nxtra Data, which is prepping for data center footprint expansion.

Jio, Microsoft deal a win-win for both

The key to this deal is how it allows both the firms to focus on their respective competitive edge. While Jio’s scale and infrastructure clout coupled with its understanding of the Indian landscape would assist in delivering seamless connectivity, Microsoft will focus on what it does best – developing and deploying its Azure cloud and AI solutions, on Jio’s network. The deal would also allow Microsoft to grow its cloud market share in India, a key point considering that cloud has now grown to become Microsoft’s biggest business segment by revenues, and is looking at India as a market to boost this growth further.

Jio, on the other hand, will bank on Azure’s brand of solutions to help persuade Indian enterprises to switch from the cloud platforms of Amazon, Google, and Alibaba, onto Azure-backed Jio’s network. Besides, Jio’s quest to explore and build high-growth businesses beyond telecom complements its decision to venture into cloud.

Key deal disruptors – ‘pricing’ and ‘native language compatibility’ – to benefit target market, and unsettle rivals

India being a price conscious market, Jio’s strategy is apparent – triggering a price war by aiming at the bottom of the ‘enterprise pyramid’, primarily comprising the startup ecosystem and SMEs, without compromising on solutions’ quality while leveraging Microsoft’s Azure brand. Jio will offer ‘free’ connectivity and cloud infrastructure to promising startups, and SMEs will be offered customized and bundled solutions encompassing connectivity, productivity and automation tools starting at just INR1,500 (US$21) per month. Similar solutions offered by rivals such as Amazon and Google can cost ~10x that price.

In addition, the Jio-Microsoft duo is looking to plug a key void left by the existing peer offerings for SMEs, i.e. local language compatibility. Jio will leverage Microsoft’s speech and language cognitive services to provide cloud and digital solutions supporting major Indian languages. This could prove to be a game-changer in a market with such language diversity as India. Local language support will likely boost broader adoption among SMEs who still largely cater to the needs of native regions.

These developments are surely going to hurt the existing cloud players, especially Amazon, Google, and Alibaba, who have a lot to ponder on countering Jio-Microsoft threat. Amazon, which has a sizeable SME clientele in India, faces the maximum risk as scores of SME customers are expected to switch from its cloud platform. Alibaba, a Chinese operator, may try to counter the Jio-Microsoft pricing but privacy and political concerns may push customers to Jio.

So how will the peers respond?

It is clear that Jio is looking to replicate its telecom price war success story in the cloud space, i.e. by offering free and discounted cloud solutions which will eventually force bigger peers to match tariffs while pressing smaller rivals to go out of business. Amazon, Google, and Alibaba will, thus, likely come up with bundled connectivity solutions at cheaper rates. Another likelihood is more webscale partnerships with local telco operators. Airtel, which already operates data centers through Nxtra Data and is on an expansion spree across India, could well be the beneficiary. But it remains to be seen if these efforts by peers are competitive enough to keep the Jio-Microsoft duo at bay. Jio’s mobile rivals are still struggling to recover from its disruption of telecom. At the least, the Jio-Microsoft partnership will help accelerate India’s cloud adoption and digital transformation.

In the last few years the demands from webscale network operators (WNOs, Figure 1) on transmission network architectures have changed considerably. From pure raw capacity requirements and lower costs, webscale players now prioritize highly scalable and advanced point to point bandwidth bundling interface technologies.

Figure 1: List of Webscale Network Operators (WNOs)

Source: MTN Consulting, LLC

Webscale operators’ field of expertise is the data center, and most planned at least initially to rent capacity as leased lines from telcos (or telecommunications network operators, aka TNOs). However, many TNOs did not have the end to end transmission networks able to support webscale needs in terms of capacity, latency, cost objectives. Further, telco networks were not flexible enough to follow rapidly WNOs’ needs for modifications, additions, and changes of the services they needed.

Hence several years ago, WNOs themselves decided to build their own backbone and regional transmission networks, sometimes linking continents. Undersea, the WNOs either leased capacity from existing submarine consortia systems or started to build submarine cables for their own dedicated use. The largest WNOs, such as Microsoft, Facebook and Alphabet, have increasingly favored the latter (self-build) approach. With these initiatives, WNOs seek to have full control of the transmission network, and adequate time to market for their needs.

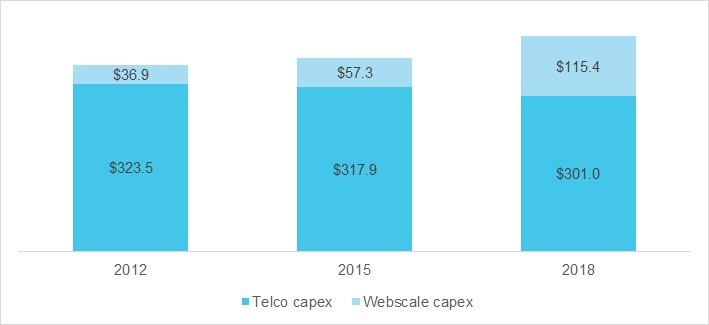

As webscale players have built out their networks, they have become more influential across the industry. Their buying power alone is a major reason; Figure 2 shows how webscale operator capex has grown dramatically since 2012, while telco capex has stagnated.

Figure 2: Capex – telco vs webscale (US$B)

Source: MTN Consulting, LLC

At the same time, the telco market is far larger, and the largest integrated telcos spend well over 10% of capex on their transport networks. These telcos are heavily investing in the transformation of their transport networks, and supporting 5G is a central goal.

In the past, mobile services have been sold on the back of convenience of use. With very little considerations beyond coverage and without a capacity objective, there was never a firm commitment to service quality. 5G is probably the first access network with services subject to a wide variety of SLAs, from best effort to non-congested, and very low latency services with limits as low as 1ms. 5G will help operators to move from best effort services for all, to a tiered service level agreement (SLA)-based portfolio. Telcos hope this will help them to be more profitable, at least for the more sophisticated services.

Network slicing poised to play important role

The big change in direction in the strategy of transmission networks is that the planning, design, engineering and operations of a telecom operator will soon be subject to much tighter contracts and commitments.

For years, wild overbooking levels have been the norm, especially for mobile services, and networks were in most cases engineered for coverage alone. This won’t be possible for the next generation of services, which will require more than a 10x increase in bandwidth, and 10x less latency than the current generation.

In addition, webscale operators and large enterprises have demanding network KPI requirements. To serve this market, telcos must develop their transmission network end to end with enough flexibility to satisfy the capacity growth needs and resiliency requirements of these customers.

TNOs and WNOs both accept that the demanding requirements on bandwidth, latency and operational scalability to ensure short time to market for 5G services cannot be supported with existing network architectures.

A potential solution is “network slicing”, which starts with adding more TDM capabilities in the data plane to be able to provide a hard separation in the way services with different KPIs use network resources. This separation is orchestrated by an SDN centralized control and management plane.

Network slicing brings improvements to traffic engineering, with clear KPIs for bandwidth, latency and packet congestion. That helps to support all types of services over the same network infrastructure. Low priority services such as web browsing are effectively separated from network resources dedicated to services with demanding SLAs such as low latency leased lines or 5G inter-vehicle communications.

Operators pursuing FlexO technology to help cope with looming Shannon limit

Historically the main requirements telcos have standardized for transmission network architectures and platforms are high resiliency, powerful operations administration maintenance features, multiservice support, and backwards compatibility with legacy platforms.

This makes a lot of sense as most of the costs of running the network are operational in nature, such as repairs and maintenance. Further, multiservice capabilities can facilitate the migration of legacy services to newer platform. This reduces the need to support overlaid networks, and also avoids the cost of capacity expansions on older platforms at or near their end-of-life (EOL) dates.

In recent years, technological developments have pushed transmission networks towards the limit in the bandwidth per distance product, or the “Shannon limit”. The transmission technology is starting to hit the limits of the fiber medium.

One way to cope with this comes from the ITU, with its Flexible OTN, or FlexO, standard (G.709.1/Y.1331.1). FlexO allows client OTN handoffs above 100Gbps by defining an “OTUCn” modular structure: “an aggregate OTUCn (n ≥ 1) can be transferred using bonded FlexO short-reach interfaces as lower bandwidth elements.” FlexO also supports standard 100GbE optical modules.

FlexO has led telcos to consider how to fully exploit the flexibility of coherent transmission systems, allowing very high capacity transmission on non-regenerated short links, say 400Gbps links over 300Km distances, and lower capacity transmission over longer links, for example 100Gbps over 1500Km distances (figures for illustration only).

FlexO can bundle a number of lower rates at the TDM level to serve a higher capacity service for very long distances. For instance, by using inverse multiplexing or bundling a 400G service interface, capacity could be carried over four 100G links over (for instance) 1500kms without regeneration.

True to their backwards compatible requirements, telcos have made sure that FlexO supports 100G transmission requirements, and is an extension of existing OTN standards. This should simplify the roll out of FlexO on existing platforms.

FlexE to improve utilization, end-end manageability and router-transport connectivity

Operators – both telco & webscale – have also been exploring breakthroughs in the interfaces between transmission systems and servers and routers.

Aligned with FlexO, the Optical Internetworking Forum’s Flexible Ethernet (FlexE) supports similar schemes of bundling and multiplexing of interfaces between routers and transmission systems. FlexE offers a way to transport a range of Ethernet MAC rates whether or not they correspond to existing physical (Ethernet PHY) rates. Network utilization should improve, as should end-end manageability. One key element of FlexE was that Ethernet would grow within a TDM frame. This may pave the way to network slicing through the use of hard boundaries between tranches of services with different SLAs.

Most webscale operators lack an access link to the end user, making them rely heavily on telcos. And smaller webscale players like Netflix rent their clouds from other providers. Maintaining control of the user experience is an uphill battle. FlexO and FlexE help achieve this, in theory. On the UNI side, a WNO transmission network would now use FlexE interfaces with data platforms and servers and storage. On the NNI side, towards the fiber and other transmission systems, the WNO would use FlexO interfaces and standards.

Transmission interoperability improving due in part to the webscale push

Interoperability is something that transport engineers always wish for but never achieve due to network management interfaces’ lack of interoperability. Further, with coherent transmission, there is a problem with transmission interface incompatibility between vendors, each of whom can be more interested in higher performance and features differentiation than simplicity.

The telco response to the interoperability challenge has generally been to achieve subnetwork level interoperability rather than network element interoperability outright.

Things will change, though, as FlexO could be called the first optical standard that thrives on multivendor equipment operations.

Furthermore, webscale operators have designed simple transmission platforms and aimed to use cheap components already available from larger industries. Examples include the use of Ethernet interfaces components at 25G and 50G that were originally proposed for intra data center connectivity and rack cablings between servers and top rack unit switches. These will also be used in 5G base stations and mobile cloud engine platforms that require a transmission network to interconnect.

Conclusions

There is a growing alignment in the requirements for transmission network architectures across telecommunications and webscale network operators. They both need more flexible ways to grow their networks and manage them on an end to end basis. They want to benefit from low cost, open source components and procurement, but adapt technology to suit their customer base. They need to be able to support different classes of service and traffic. Even when providing free services, operators need to deliver a high quality of experience in order to monetize.

5G transport and data center interconnectivity services pose such a challenge to both TNOs and WNOs that work-arounds will not make up for limitations in either the data centers nor the network. For many operators, building a transmission network that supports network slicing principles will require a fresh start and new investments.

–

Source of cover image: CommScope.

[Note: a condensed version of this article first appeared at Telecomasia.net.]

Whether you’ve joined the #deletefacebook camp or not, it’s hard to deny that Facebook has dug a deep hole for itself this time.

Yesterday’s NYT report was a harsh assessment of the company’s trustworthiness. It’s worse when combined with the late September news that Facebook had “exposed the personal information of nearly 50 million users”. These two reports – and a range of more brutal looks at the company – highlight the risks of trusting any large company with your data, much less the volume and sensitivity of data which Facebook demands. For a company that relies almost entirely on advertising for revenues, this is serious.

Immensely profitable. Still.

Let’s not cry for Facebook though. It has had an incredible run. The company’s 12 month revenues have grown from under $30B in 2016 to over $50B for the period ended September 2018 (figure); even the relatively modest 31% YoY growth recorded in 3Q18 far outpaces most tech companies.

Facebook’s growth has delivered high profitability rates, whether measured by net margin (38% annualized in 3Q18) or free cash flow to revenues (34% in 3Q18). Its excess cash has allowed it to invest in both capex and internal R&D at relatively high rates. Facebook’s capex deployment ratio (capex to revenues) is now higher than most telecom operators, at 23%.

You could also argue that Facebook’s high rates of proprietary tech investments (R&D) and capex spend on strategic infrastructure (mostly data centers) have driven earnings – not the other way around. In reality, it’s probably been a virtuous circle for FB so far, but that has always remained dependent on its incredible growth rates in usage and ad dollars. As Facebook’s advertisers see millions of users quitting or spending less time on the platform, clicking on fewer ads, and turning fewer of those clicks into transactions – they will find new outlets. Amazon is counting on it, in fact, with its recent foray into ads, and it’s been successful so far.

As the figure above hints at, Facebook spends big on the network infrastructure behind its business: for the first nine months of 2018, its capex on Network, IT & Software was $4.47B, about half of the company’s $9.6B total capex. Any slowdown in growth will eventually hit network spending.

Even if Facebook does some development in house, now including chips, it still buys lots of tech (hardware and software). Some companies & markets to watch:

Servers: Facebook works with several contract manufacturers in Taiwan for production, including Quanta Computer, Wistron, and Wiwynn. These companies may see the effects of any slowdown first, if new server orders fall due to slower traffic growth rates, and/or new data center opening dates are delayed.

Chips: as discussed in a previous blog, Facebook made the big decision to self-develop earlier this year. That offers a modest competitive threat to Nvidia, Intel, and Qualcomm. The economic and operational incentive to keep building its own chips hasn’t gone away since then. If any privacy concerns can be unearthed in the chip area, though, Facebook will certainly face them. More interesting is potential impact on Qualcomm. Facebook uses Qualcomm’s chips for the social media’s rural connectivity project, Terregraph. This program could be at risk, even after recent trials in Hungary, Malaysia, and Indonesia.

Subsea communications: Facebook is a founding investor/owner of five major submarine cables: Argentina-Brazil with Globenet, two transatlantic cables (MAREA and HAVFRUE) and two transpacific cables (JUPITER, and PLCN). These projects have long planning cycles and probably would not be affected by a FB slowdown. However, Facebook’s current search for the right cable investment in Africa may be delayed, or require more partners (Google, Microsoft and Amazon are also looking at the region)

Optical components: Lumentum, NeoPhotonics, and Applied Optoelectronics are FB’s main OC vendors; for the same reasons cited above, they could face some volatility in demand from Facebook.

Earnings calls over the next few weeks may be revealing.

Rumors about Facebook’s likely entry in the hardware segment were put to rest after the company posted job openings for chip designers. Facebook was looking for candidates specialized in architecting and designing ASIC and FPGA chips, to help build “custom solutions targeted at multiple verticals including AI/ML, compression, and video encoding.” Facebook has data center applications on the mind, such as live video content filtering, but the company may also be building chips to support its Oculus virtual reality headset and long-planned smart speaker.

Facebook’s chip plans are risky but may bring increased control over supply chain

Facebook’s recent move to make its own artificial intelligence (AI) chips and get a foothold in the hardware segment is a step in the right direction, as it looks to reduce dependence on chip manufacturers (Intel, Nvidia and Qualcomm) while putting a lid on its costs. However, designing a chip is by no means a simple task and not a core competency at Facebook. Matching the performance and efficiency of Intel, Nvidia and others will be a challenge.

Why would Facebook take the risk? It’s loaded with cash ($41.7B in Dec 2017) and used to making high-stakes tech investments. But the chip market is competitive, and Facebook has substantial buying power – it could certainly rely on the open market. Time to market may improve with self-design, for sure. However, another benefit may be more persuasive: Facebook gets greater control over intellectual property rights and information flow. It likely has a few surprises in store.

Big technology investments needed to support social networking

Facebook’s growth has been driven by acquiring and strengthening complementary services to its social networking business, such as WhatsApp and Instagram. Supporting this growth enticed Facebook to build a huge core network.

Like other webscale providers, Facebook works with contract manufacturers to build custom servers and other gear for their massive data centers. Facebook has played an important industry role in this regard, serving as an early sponsor for both the Open Compute Project (OCP) and Telecom Infrastructure Projects (TCP). Now Facebook is testing the waters in consumer electronics markets, initially with its Oculus virtual reality headsets, a smart speaker to be launched in 2018, and complementary AI software. These efforts have contributed to both high capital spending and R&D expenses at Facebook (Figure 1).

Facebook believes that creating its own custom designed chips will result in better integration of hardware and software, and give it tighter control over the development of the product. One factor behind Facebook’s chip push is an interest in running AI algorithms in-house, to avoid sharing with third-party vendors like Intel or Qualcomm. Not every webscale company can do this, but Facebook is positioned better than most due to its deep capex budget & its pioneering work at the OCP, TIP, and other groups.

Working in Facebook’s favor is its recent partnership with Intel to manufacture its own AI processor last year.

Impact of Facebook’s entry into the semiconductor space on the big chipmakers

In the past two years, there has been growing tension between the tech players building cloud networks and the vendors they rely on, mainly Intel, Qualcomm, and Nvidia. Historically the largest cloud builders, “webscale network operators” (WNOs) in our terminology, have heavily relied on Intel’s microprocessors and Nvidia’s GPUs to power their data centers (Figure 2).

However, Facebook is not the only WNO to look at building its own chip. Many webscale providers are starting to look in-house to build custom AI chips to reduce costs and improve on efficiency. For instance, Google developed an AI chip, Cloud Tensor Processing Unit (TPU), two years back, to boost its AI workloads. Google released a latest version this month, indicating that Nvidia’s dominance as a supplier of AI chips could soon be in jeopardy. Similarly, Apple plans to build its own chips for its Mac desktops by 2020, thus reducing its dependence on Intel. Amazon is building its own custom hardware to improve its Alexa enabled devices. Microsoft has launched a new cloud service for image-recognition projects powered by its FPGA technology, codenamed “Project Brainwave”. This will rely on Intel Stratix 10 chips and support a neural network based on the ResNet-50 architecture. Microsoft claims that this new technology will be capable of handling AI tasks rapidly enough to be used for real-time jobs and at a reduced cost in comparison to the graphics chips (e.g. NVIDIA) used in machine learning tasks.

As webscale tech players build more of their own chips, traditional chip developers are getting nervous.

One company affected in a big way by Facebook’s move is Qualcomm. Facebook’s new chips may be used to power its VR headset, Oculus Go, which currently runs on a Qualcomm Snapdragon 821 chip. This could be a huge blow for Qualcomm. And it comes at a time when Qualcomm is already struggling after its legal battle with Apple, an attempted acquisition from Broadcom, and a still-pending merger with NXP.

The chip vendor’s fears are not just theoretical. Webscale players have already had an impact on the supply chain, hurting server vendors like IBM and HPE in past years by going to white box/contract manufacturing. Now they’re big enough to design their own chips. That cuts out the middleman, avoids having to share secret IP, maybe speeds time to market, and may result in some proprietary advances.

Facebook will have to win back faith amidst data privacy scandal

While Facebook engineers will continue to find ways to make their network cheaper and smarter, the company faces more complex challenges in the area of data privacy & public perceptions.

Facebook’s privacy practices have come under global scrutiny in recent months, due to the recent Cambridge Analytica and Android call data scandals, not helped by a photo tagging-related lawsuit. As a consumer-facing brand with plans to build its own IoT hardware, a lot is at stake. The company needs to build trust and improve transparency. It cannot do this while also maximizing ad revenue growth. Not all Facebook executives seem willing to accept this.

Amid all the public outcry, the launch of Facebook’s smart speaker has unsurprisingly been delayed. With recent news that Amazon’s Alexa has some interesting privacy-related glitches, Facebook’s decision is probably best. Now seems like a good time to focus on the basics.

Top US-based tech providers Amazon, Alphabet/Google and Microsoft dominate the cloud space but they are set to face stiff competition from China’s leading cloud provider Alibaba.

MTN Consulting tracks these and similar operators of webscale (aka hyperscale) cloud networks as part of its “Webscale Network Operator” (WNO) market segment.

AliCloud launched nine years ago, now going global

Alibaba established its cloud computing division in 2009, three years after Amazon launched AWS, and went global by 2015. The Chinese company has set up data centers across the Middle East, Singapore, Japan and Europe through its cloud division (Alibaba Cloud, also known as AliCloud or AliYun). It has been ambitious from the start. In 2015, Simon Hu, President of Alibaba Cloud, predicted the company would surpass Amazon by 2019: “Our goal is to overtake Amazon in four years, whether that’s in customers, technology, or worldwide scale.”

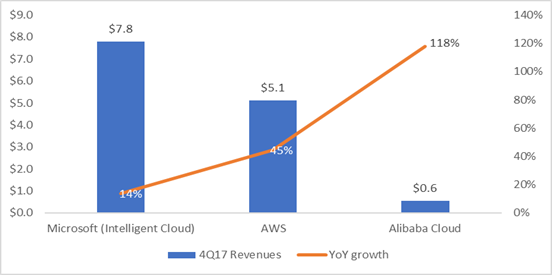

Simon’s goal may have sounded a bit far-fetched then, but with a whopping 118% YoY revenue growth from its cloud segment in 4Q17 (as shown in Figure 1), Alibaba is beginning to live up to its ambitions. While still small on an absolute basis, Alibaba has a history of rapid, aggressive expansion into new markets – it is a serious player in the cloud now.

Figure 1: Webscale network operators’ 4Q17 cloud* revenues (in US$B) and YoY growth rate

Source: company filings

Key takeaways from 4Q17 results

Fourth quarter earnings for top WNOs revealed continued strong growth overall, along with some competitive & strategic shifts. Highlights for the top few providers:

Amazon’s sales hit $60B in 4Q17, up 38% YoY, backed by strong sales in the holiday season, and its net profit was also up 148% in the same period. However, operating margins were low for Amazon’s North America segment, which in FY2017 generated just $2.8B in operating profit on revenues of $106.1B. Amazon Web Services (AWS) is a different story. AWS is Amazon’s cash cow business as it continues to generate profit for its group, despite incurring losses from its international segment. As shown in Figure 1, AWS segment’s 4Q17 revenues were $5.1B (up 45% YoY). In the same period, AWS’ operating profit was $1.35B (up 46% YoY) and was also a major contributor to the company’s overall profitability.

On an annual basis, the AWS segment recorded revenues of $17.5B in 2017, (up 43% over FY2016) and now contributes to about 10% of the company’s sales, from just 3% in 2011. AWS’ operating profit for full-year 2017 was $4.3B (with a margin of 25%), much higher than the 3% margin recorded by Amazon’s North America retail segment.

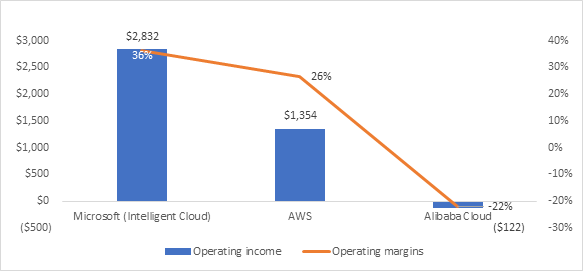

Figure 2: WNO 4Q17 cloud operating profit (US$M) and margin (profit as % of revenues)

Source: company filings

Microsoft’s revenues from Intelligent Cloud* were $7.7B in 4Q17, up 14% YoY. The majority of Intelligent Cloud revenues come from Azure, which grew by 98% during the same period. Intelligent Cloud operating profit was $2.8B, up 18% YoY, giving the division an operating margin of 36% (Figure 2). A key differentiator for Microsoft is its hybrid cloud strategy, which aims to help enterprise users exploit their legacy IT investments. It hit the right note with its acquisition last month of storage vendor, Avere Systems. This acquisition will further enhance Azure’s enterprise capabilities, as Microsoft can merge Avere’s storage capabilities into its own Azure cloud services. That will enable large and complex high-performance workloads to run in Azure.

Alibaba’s cloud computing segment recorded strong revenue growth in 4Q17 (up 118% YoY) but continued to incur losses from this division (Figure 2). In the same period, its cloud segment incurred an operating loss of RMB793M ($122M), and a negative operating margin of around 22%. Unlike Amazon and Microsoft, which generate a good chunk of profits from their cloud segments, Alibaba’s continual losses from its cloud segment are a reminder that its focus is on growth and not profitability. With a free cash flow (operating cash flow – capex) of over $7B in Q4’17, Alibaba has enough cash to plow into its cloud business.

Alphabet’s overall 4Q17 result was promising. Its 2017 corporate revenues crossed $100B for the first time, posting $32.3B in 4Q17 alone. This 24% YoY growth was mainly due to advertising and mobile search. For the first time, Google disclosed its cloud revenues, a little over $1Bn in 4Q17. That figure is lower than that of AWS and Microsoft Azure, but Google Cloud is relatively new. Alphabet has spent over $30B in capex in the last three calendar years, the bulk of which went to its data center and subsea cable network. Alphabet aims to leverage this investment far beyond search. It continues to connect new regions to its Google Cloud Platform, with data centers opening in the Netherlands & Montreal, Canada already this year. The GCP’s network now has 15 regions, 44 zones, and over 100 points of presence.

Alibaba will retain an advantage in China, and is now eyeing global expansion

The cloud computing business in China has long been dominated by domestic players, as the US tech giants find it difficult to make inroads due to the strict laws around censorship and content regulation. The recent stringent law around cross border data transfer will only make life harder for foreign cloud companies, as they are required to store data locally. That will benefit Alibaba, as well as the smaller cloud operations of Baidu and Tencent.

Further, the government restricts foreign ownership of cloud services in China, as they can provide services only via a partnership arrangement with domestic cloud providers in China. For instance, AWS is currently operating in China by partnering with Beijing Sinnet Technology (Sinnet), as AWS is banned from operating under its own brand name in China. In Nov 2017, Amazon sold its hardware to Sinnet, as the law prohibits foreign companies from owning technologies for cloud services. Along similar lines, Apple and Microsoft are currently operating in China through Guizhou on the Cloud Big Data (GCBD) and 21Vianet Group. With US cloud companies forced to wade through tricky regulatory waters in China, Alibaba again benefits.

Alibaba has invested heavily in expanding its network of data centers, and is developing its own proprietary technologies for the AliCloud (Figure 3). As part of its global expansion, India is an initial focus. This will not be easy, as Amazon is clearly the leader in the Indian market. And with Amazon’s failed attempt to flourish in China, the company has all the more reason to defend its turf in India. However, Alibaba has deep pockets and ambitions, too, as it launched a new data center in India in Dec 2017 and in Malaysia recently.

Figure 3: Self-developed infrastructure for the Alibaba Cloud

Source: Alibaba’s 2017 Investor Day.

At the recently concluded Mobile World Congress (MWC) in Spain, Alibaba made clear its intentions to compete in European cloud markets. At the event, AliCloud introduced several new cloud offerings aimed at HPC (high performance computing) workloads, and AI and other data-intensive workloads. To establish a supporting technology ecosystem in Europe, AliCloud is partnering with Vodafone Germany, the Met Office UK and Station F (a France-based startup company). Alibaba hopes to make commercial progress with these new services, and showcase its capabilities in the fields of AI and big data. Ultimately it aims to leverage innovations in these fields across multiple industries. AliCloud’s global expansion is off to a good start.

*Note: For this analysis, we have considered AWS revenue for Amazon and Google Cloud for Alphabet. For Microsoft, we considered total revenues for its Intelligent cloud segment, as the company does not report stand-alone revenues for Azure.

MTN Consulting has just published a “Market Review” of the carrier-neutral network operator (CNNO) sector. The report assesses the key role that these tower, data center, and bandwidth specialists are playing in the downsizing of the telecom sector. While many telcos are shrinking, the CNNO sector is growing >10% per year. Revenues for the 25 CNNOs we track should surpass $40B this year, and approach $60B by 2020 (Figure 1).

Takeaways from the study include:

CNNO revenue growth has been steady around 10-15% YoY for several years, in line with the growing telco (& other provider) need for low cost, carrier-neutral network resources. 3Q17 revenue growth for CNNOs was 13.1% (Telco Network Operators: 1.0%; Webscale Network Operators: 23%).

CNNO capex rose 11% YoY in 3Q17, to $3.6B. Tower specialists spent 24% of their revenues on capex, data center specialists over 43% due to higher (and lumpy) investments in developing new sites. Tower providers’ incremental capex in new sites is primarily for small cells. Bandwidth specialists’ capital intensity has been over 50% for the last 5 quarters, due to the influence of new builds (NBN in particular).

CNNO capex hit $15B on an annualized basis in 3Q17; the biggest spenders were Equinix, Level 3, Australia’s NBN, Crown Castle, Digital Realty, American Tower, and Zayo.

M&A is a big factor in the sector’s growth, but just one. CNNOs are growing organically too, and expanding their business models to require a broader mix of equipment (Crown Castle is looking at edge computing, for instance). Technology-related operating expenses can be quite high, for repairs & maintenance of old plant, and energy costs in particular.

Total capex across telecom, Webscale, & CNNO was $355B in 4Q16-3Q17 (Figure 2).

The report also assesses CNNOs’ network holdings across four main categories: fiber, data centers, towers, and small cells. Most big operators have assets in multiple areas, and that will increase over time. Tower companies are building small cells, for instance, while bandwidth specialists are extending their fiber routes to small cell sites.

Table 1 provides a snapshot of the infrastructure assets for a sample of the CNNOs covered in this report.